Real yields at 2% are too good to pass up. Or am I wrong?

By David Enna, Tipswatch.com

OK, it’s a silly headline. I am not really day-trading in the Treasury and fixed-income markets; I’ve only been buying and not selling. But I have dramatically stepped up purchases in the last four months.

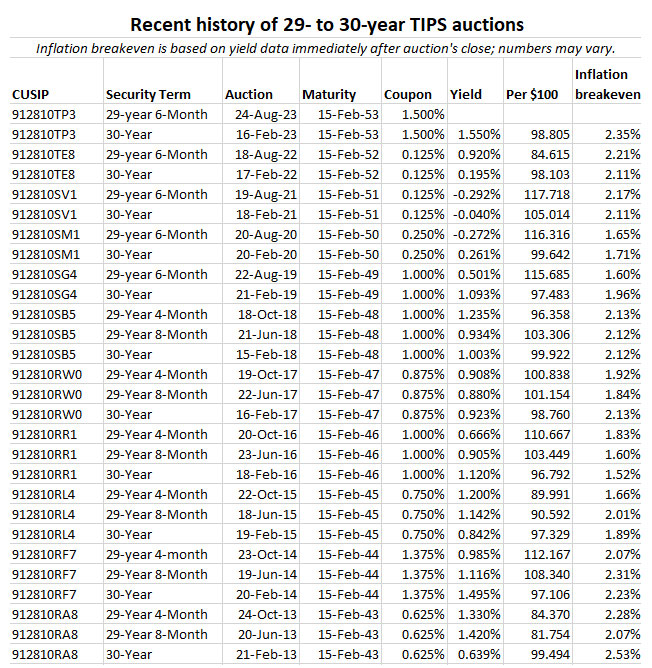

All this started in mid-2022, as the Federal Reserve began ratcheting up short-term interest rates. At that time, I worked out a strategy to space out purchases of 13- and 26-week Treasury bills and then roll the investments over, always allowing access to part of the money within 4 weeks. I wrote about that strategy in July 2022 and followed up in August 2022. Those investments are still rolling over, now yielding 5.5%+.

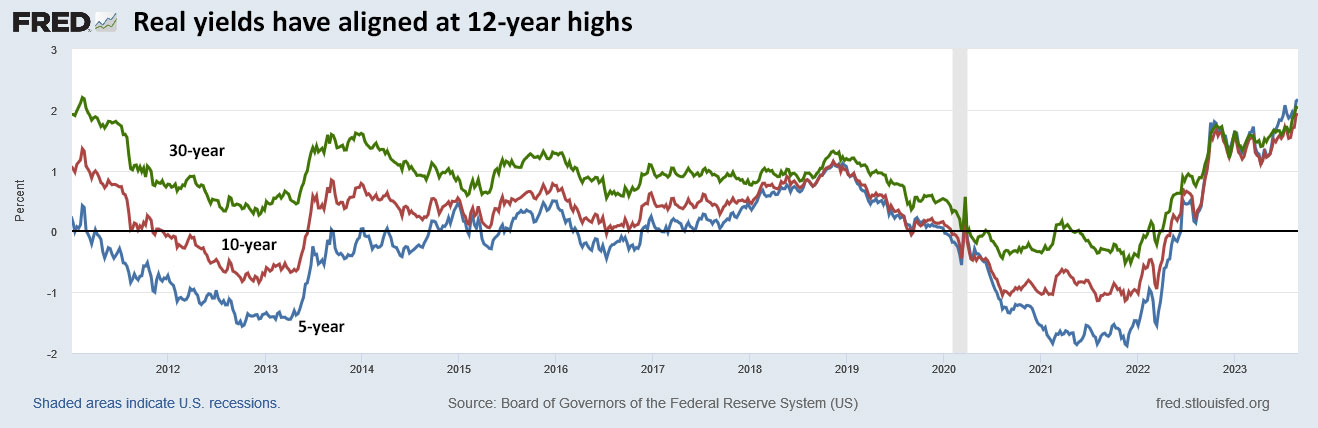

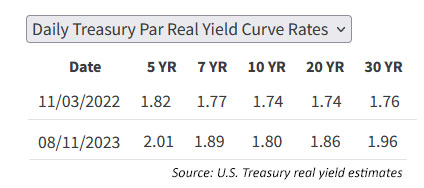

At the same time — mid 2022 — I began liquidating my holdings in Schwab’s U.S. TIPS ETF (SCHP) and very gradually began using that money to buy individual TIPS, both at auction and on the secondary market. Real yields were rising, finally, and by November 2022 had hit decade-plus highs. Unfortunately, that trend reversed in the early months of 2023, with the 10-year TIPS real yield falling from 1.73% on Nov. 3, 2022, to 1.06% on April 4, 2023. So my buying spree slowed down.

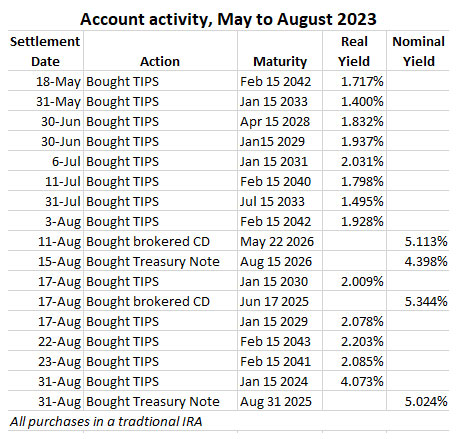

Fast forward one month to May 2023 and real yields again began rising, up more than 40 basis points by the end of that month. So I began buying TIPS again, and a bit more aggressively. As it turned out, a new strategy formed: to build a TIPS ladder through the year 2043, with near-equal amounts in each year. To do this, I began liquidating my holdings in Vanguard’s short-term TIPS ETF (VTIP).

I’ve been doing this in a traditional IRA brokerage account at Vanguard, so taxes are not an immediate concern. My strategy combined buying longer-term TIPS (5 years or longer) combined with some nominal investments in the 2- to 3-year range, to prepare for paying future RMDs from this account. Plus I will need investable money in 2024 through 2029 to buy 10-year TIPS in each of those years to complete the ladder. (There are currently no TIPS maturing from 2034 to 2039.)

Here is what I have been doing since May 2023:

My ladder-building strategy is nearly complete, but I am still looking to fill out the years 2040 to 2043 with amounts equal to the earlier years. I am hoping to nail down 2.0%+ real yields for each of those investments in coming weeks. Some days I can find them on the open market; most days I can’t.

On the nominal side, I have been looking for decent yields to provide cash in my early RMD years (2026 and 2027). This IRA account also has a 20% holding in Vanguard’s Total Bond ETF (BND) and 20% in Vanguard’s Wellington Admiral (VWENX). So I have some flexibility for those future RMD withdrawals.

And I should point out that about 10% of my TIPS are old-school purchases that remain in a taxable account at TreasuryDirect. All those, except one, will roll off by 2029.

What is the strategy?

Any investment can look dumb in a few months. I could have been in cash for the last 12 months and just bought all these TIPS at the top of the yield cycle last week! But here’s my advice: When you are putting your money into a very safe investment with a known decent return: Buy without regrets. When you see real yields that are historically attractive, go ahead and invest. As long as you have a plan.

Yields could keep going higher, obviously. Maybe even much higher if you take a dire view of the U.S. borrowing needs in the next few years. Site reader Amit this week provided a link to this video, laying out a very bearish view of the U.S. bond market:

I have no idea who these guys are or anything about their “All-In” podcast, but the speaker, David Friedberg, makes valid points about the potential extreme level of borrowing needed to fund U.S. deficits in the near future. That could lead to higher nominal yields, which would also drag real yields higher, most likely.

So there is always the possibility that buying at today’s decade-high real yields could look bad into the future. But because these investments are Treasury Inflation-Protected Securities, if held to maturity they will deliver a return of about 1.8% to 2.0% above inflation. That is a certainty.

These investments are part of an asset allocation in a single account — a traditional IRA — that just needs to keep pace or exceed U.S. inflation for the investments to provide what I need: A stable flow of cash until I reach age 90. So I am buying now to lock in that real return, an opportunity we didn’t have in the decade-long stretch of ultra-low yields.

I know a lot of readers are also adopting this “safe-withdrawal” strategy, first promoted by financial author Allan Roth in his October 2022 article, “The 4% Rule Just Became a Whole Lot Easier.” This strategy, as Roth notes, is only possible when real yields are above 1.7% — the range we are seeing today.

So with that in mind, I have been acting to build this ladder of very safe TIPS investments through 2043. It’s not day-trading, but it has become an obsession, I’ll admit.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Like most, most think there may be a legislative solution and what that may be...there could be no legislative solution!…