Shorter-term rates will fall. The future of longer-term rates is uncertain.

By David Enna, Tipswatch.com

Just a few days ago, on Aug. 22, the U.S. Treasury auctioned a reopened 30-year Treasury Inflation-Protected Security with a real yield to maturity of 2.055%. And then, a day later, a lot changed. Did we just see — for the time being — the last TIPS auction with a real yield higher than 2.0%?

It could be. Bond markets shifted mightily in the aftermath of Federal Reserve Chairman Jay Powell’s short, but very direct, speech Friday to the Jackson Hole Symposium on monetary policy. Watch it here:

Some key quotes:

Inflation has declined significantly. The labor market is no longer overheated, and conditions are now less tight than those that prevailed before the pandemic. Supply constraints have normalized. And the balance of the risks to our two mandates has changed. …

The upside risks to inflation have diminished. And the downside risks to employment have increased. …

The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks. … With an appropriate dialing back of policy restraint, there is good reason to think that the economy will get back to 2 percent inflation while maintaining a strong labor market ….

The limits of our knowledge—so clearly evident during the pandemic—demand humility and a questioning spirit focused on learning lessons from the past and applying them flexibly to our current challenges.

My reaction: “Hell of a speech.” Why? Because Powell clearly laid out the Fed’s plan to begin lowering interest rates (probably 25 basis points next month) and also implying that the decade-long period of aggressive monetary stimulus was a “lesson in consequences.” Now that the U.S. is recovering from a 40-year high in inflation, Powell’s reference to humility was appropriate.

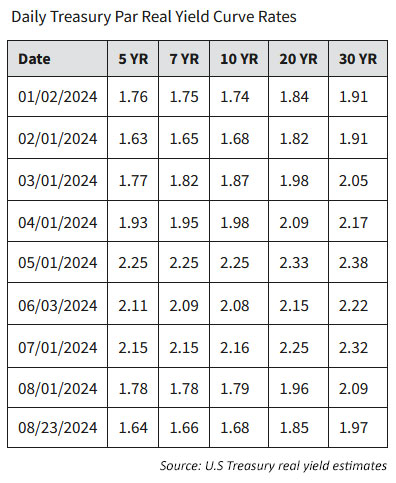

Powell’s speech set off a strong rally in both U.S. stocks and bonds, with Treasury yields falling across all maturities. The 30-year TIPS that auctioned Thursday with a real yield of 2.055% closed Friday at 1.97%. Not a huge move, but the fall in shorter-term maturities was more dramatic, with the 5-year TIPS real yield falling 12 basis points in a single day.

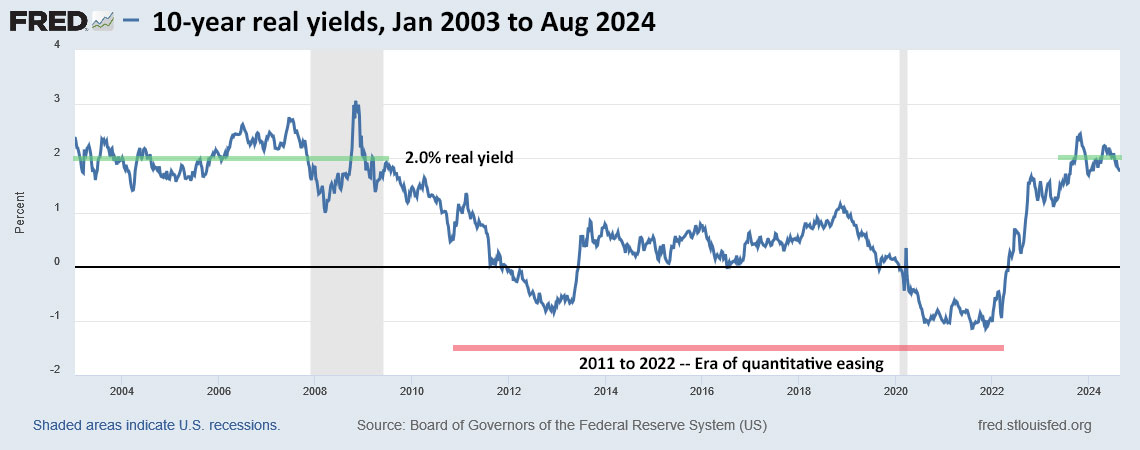

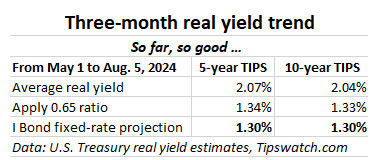

At Friday’s market close, the full spectrum of medium- to long-term TIPS closed with real yields below 2.0%. I think that is significant because 2.0% is an attractive historic target for TIPS purchases. Take a look at the trend in 10-year real yields over the last 21 years, showing how rarely investors could hit that 2.0% mark over the last 14 years:

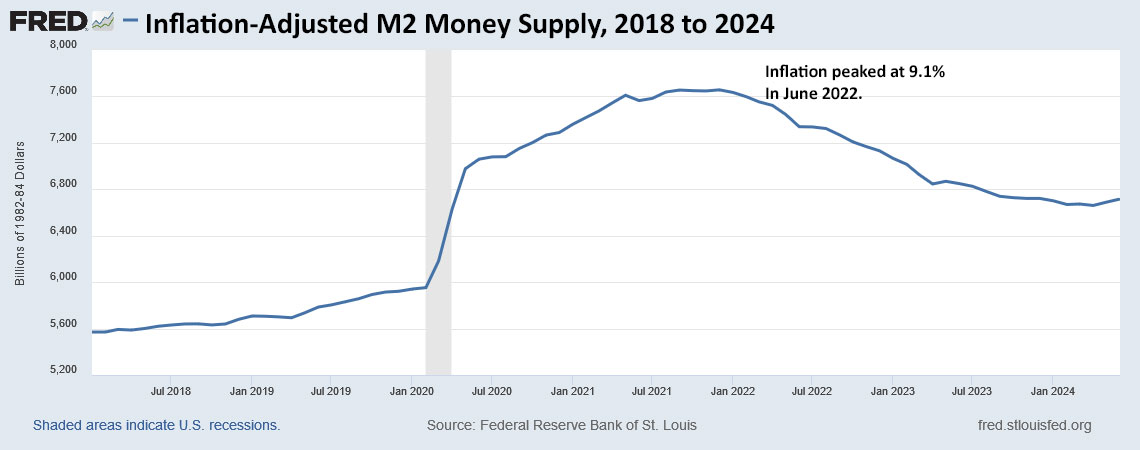

On the above chart, I have noted the years of the Fed’s moderate to aggressive policy of quantitative easing, which was openly forcing Treasury yields lower. That policy could continue while inflation remained under control, as it did for years. But then came the 2020 pandemic and severe economic distress. The Fed and Congress acted together to flood money into the U.S. economy at a time of severe supply disruptions, creating the rather obvious potential for high inflation.

A new era of the new era

Because of the humbling lessons learned, I believe the Fed isn’t going to shut down its focus on controlling inflation even if the U.S. economy slips into a sight decline. So that means medium- to longer-term interest rates could continue near today’s fairly high — but normal — levels for some time. But shorter-term rates will decline as the Fed moves to lower its federal funds rate by 150 to 200 basis points over the next 18 months.

One predictable effect of declining U.S. interest rates is a matching decline in the value of the U.S. dollar, as foreign investors shift some bets to other currencies. The U.S. dollar has fallen more than 5% since late June. The end result of that should be –eventually — somewhat higher U.S. inflation, which in turn should stabilize longer-term Treasury yields.

One potential effect of a weaker dollar would be higher oil prices, but so far we haven’t seen much of an effect, possibly because of the potential of weaker international economies.

Real yields have been volatile throughout 2024, and I would expect that trend to continue, while potentially sinking lower.

So, in my opinion, we could see 20- to 30-year real yields at times again rise above 2.0% even as the 5-year real yield sinks lower. The yield curve is steepening and that should continue. Keep in mind that the U.S. Treasury needs to continue to issue debt to cover massive U.S. deficits. If the Fed isn’t buying that debt, market forces should result in stable or higher longer-term interest rates.

Back in February 2010, when the Treasury resumed issuing 30-year TIPS, the yield curve was quite steep, with the 5-year TIPS yielding 0.55%, the 10-year at 1.55%, and and the 30-year at 2.22%. Was that normal? It seemed like it at the time.

In summary, I think we are entering a time of almost certainly lower short-term interest rates and murkily uncertain medium- to longer-term yields. A lot will depend on the fate of the U.S. economy and what actions the Fed would take if things again hit “crisis mode.”

As Powell said Friday, “That is my assessment of events. Your mileage may differ.”

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep or the display breaks on the mobile site. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I thought he was cagey and cryptic. The manifest content of what he said, along the lines of "inflation is…