Are they a steal? Not really.

By David Enna, Tipswatch.com

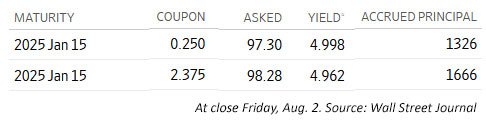

Recently, I have been getting questions and comments about the two Treasury Inflation-Protected Securities maturing on January 15, 2025. These are quoted on the secondary market as having eye-popping real yields close to 5%.

For example, here is a comment from July 31:

A nominal note (91282CDS7) maturing on January 15 has a YTM of 5.041. The TIPS (912828H45) has a YTM of 5.038. Does that mean if inflation is 0.003% or higher the TIPS will be the better investment? It looks like a steal to me. Am I missing something? Isn’t CPI over 2%? Is the seasonal adjustment going to be -2%?

This issue comes up every year for the TIPS maturing in January because of two oddities of TIPS: 1) After July 15, a TIPS maturing in January has only one coupon payment remaining, and 2) The principal balances for these TIPS are highly likely to get hit by a deflationary month (or two) before maturing. That is likely because TIPS accruals are based on non-seasonally adjusted inflation, which always runs lower than seasonal CPI toward the end of the year.

In 2023, for example, non-seasonal inflation was -0.04% in October and -0.20% in November. Since 2012, October non-seasonal inflation has been negative in 6 of the 12 years. November inflation has been negative 10 of the 12 years.

By market logic, the ending nominal yield for a TIPS purchased today and maturing in January should be close to a T-bill purchased today and maturing in January. Except that with the TIPS, there is a risk of under-performance that is not a factor for the basically riskless T-bill.

For example, last year I made an experimental purchase of CUSIP 912828B25 – maturing in January 2024 – to see how its real yield of about 4.0% would compare with a nominal T-bill of the same term. In that case, the TIPS ended up being the winner versus the T-bill, with an annualized nominal return of 6.2% vs. 5.5% But that won’t always be the case. Some things to consider:

The coupon rate is diminished as a factor.

Both CUSIP 912828H45 and 912810FR4 have only one coupon payment remaining, to be paid on Jan. 15 on the ending principal balance. For H45, the last payment will be 0.125%. For FR4, it will be 1.1875%. It is important to realize that once you purchase a TIPS, your return at maturity will be par value x final inflation index + final coupon payment.

Notice that even though the two TIPS have a wide variance in coupon rate, the current ask price is now quite close — 97.94 vs 98.93. That gap will continue to narrow as we approach Jan. 15, 2025.

The discounted price is key to your return.

If you buy a TIPS with a price of 97.94, you are getting a discount of 2.06%. At maturity, the price will be 100 — par value. If you annualize 2.06% from 5.5 months to a year, you get a nominal return of about 4.55%. The discount, not the coupon rate or upcoming inflation, is the major factor determining your eventual return.

In essence, purchasing a very short-term TIPS is much like purchasing a zer0-coupon bond (or a T-bill, which is originated at a discounted price.)

These TIPS have high inflation accruals.

H45 currently has an inflation index of 1.32602, meaning an investor will be purchasing 32.6% additional principal above par value. FR4 was originally issued on July 15, 2004, as a 20 1/2-year TIPS, so its inflation index is much higher — currently 1.66620. So in this case an investor will be purchase 66.6% additional principal above par value.

Purchasing a very short-term TIPS with a high inflation accrual creates some risk, because only par value is guaranteed to be returned at maturity. That is especially true for a TIPS maturing in January or April, because these TIPS are likely to get hit by a deflationary month near the end of their terms.

A potential scenario

Both of these TIPS already have an inflation index set through August 31, based on June’s meager non-seasonally adjusted inflation of 0.03%. And then …

- July inflation will set September inflation accruals.

- August inflation will set October inflation accruals.

- September inflation will set November inflation accruals.

- October inflation will set December inflation accruals.

- November inflation will set inflation accruals through January 15.

I have no idea of where inflation is heading through November 2024, but I do feel confident there could be one or two deflationary months in that mix. And that, I believe, is also what the market is expecting.

In this scenario, I am reflecting market expectations, which appear to be for fairly low non-seasonally adjusted inflation through the end of 2024. Here is how a $10,000 par purchase for these two TIPS works out, using these conservative estimates:

One qualification on the annualized yields: Almost all of the yield advantage for the two TIPS comes from the fact they have a 5.5-month term versus 6 months for the T-bill. In other words, the dollar returns would be similar, but the TIPS get there quicker.

In the end — under this inflation scenario — both TIPS would out-perform a 6-month T-bill. If inflation runs higher, each TIPS will do better. If harsher deflation sets in, the TIPS will under-perform. The TIPS investment involves some risk, while the T-bill is essentially riskless. For that reason, it is logical that the TIPS would provide the higher potential yield.

Conclusion. Unless you expect inflation to surge higher at the end of this year, the T-bill still looks like the more sensible, much-less-complex investment. That’s my opinion.

—————————-

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I liked the results... added a little more of this issue.