By David Enna, Tipswatch.com

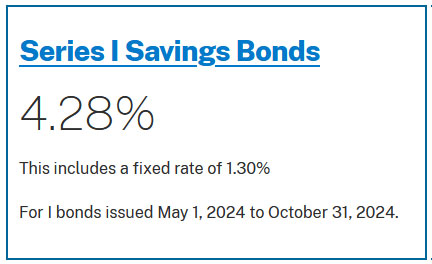

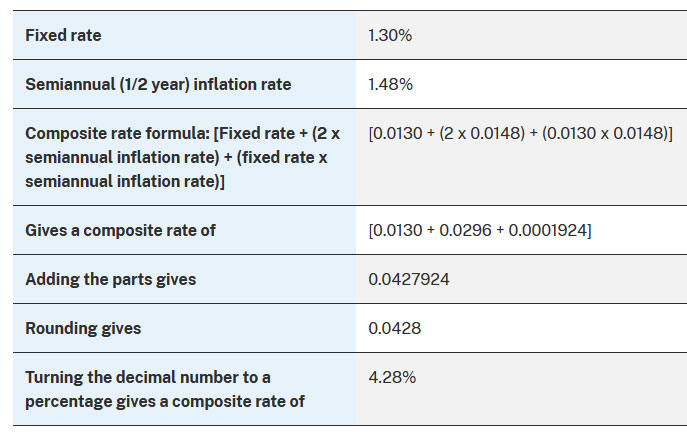

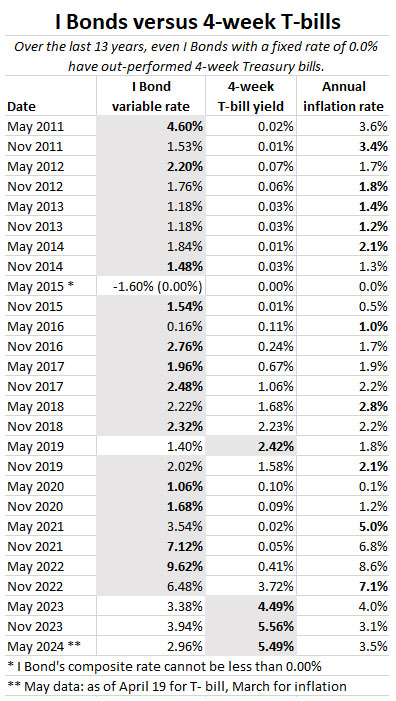

Last week, the Treasury set the fixed rate for I Bonds purchased from May to October 2024 at 1.3%, which combined with a variable rate of 2.96% results in a composite rate of 4.28% for six months.

As it turns out, that 4.28% composite rate also applies to I Bonds purchased from November 2023 to April 2024, because those also had a fixed rate of 1.3%. But what about I Bonds purchased in previous years, with fixed rates as low as 0.0%?

All I Bonds — no matter when they were purchased — will have the inflation-adjusted 2.96% variable rate applied for a full six months. The starting month depends on the original month of purchase, following this chart from TreasuryDirect:

For example: If you bought I Bonds in January 2024, that investment will earn a composite rate of 5.27% for six months, and then in July will begin earning 4.28% for six months. A purchase in April 2024 will earn 5.27% for six months, and then in October begin earning 4.28% for six months.

But what about those earlier I Bonds in your inventory, with much lower (or possibly higher) fixed rates? Any I Bond with a fixed rate of 0.0% is going to earn the variable rate, with no added fixed rate. So those will transition from earning the previous variable rate of 3.94% for six months to 2.96% for six months.

In this chart, I have compiled the new composite rates (which will roll into effect based on the original month of purchase) for all I Bonds back to November 2016, and then selected I Bonds with varying fixed rates back to May 1999. The chart also shows the current value of these I Bonds, assuming the I Bonds were purchased in the first month of each time period:

Note that the May 1 value shows total interest earned, ignoring the Treasury’s three-month penalty for redemptions before five years.

Thoughts

Because of the inflation protection built into I Bonds, earning 2.96% for six months isn’t a dreadful thing. Get over it! But … at a time when 4-week Treasury bills are yielding 5.47%, that 2.96% is looking weak. You can reach a similar conclusion with other low fixed rates:

- A fixed rate of 0.10% will generate a composite rate of 3.06% for six months.

- 0.20% = 3.16%

- 0.30% = 3.26%

- 0.40% = 3.37%

- 0.50% = 3.47%

- 0.70% = 3.67%

As I have written recently, this year I have redeemed 0.0% I Bonds to purchase the new 1.3% I Bonds, both in the traditional way in March and in gift-box swaps in April. I still have one set of 0.0% bonds remaining (from 2017) and a rather large collection of 0.1% fixed-rate I Bonds dating back to 2013.

At this point, I would not redeem any I Bond with a fixed rate of 0.2% or higher.

Also in the chart, notice the I Bonds issued from May to October 2007 with a fixed rate of 1.3%, same as today’s. Those I Bonds are very close to doubling in value in 17 years. They have generated a tax-deferred, annualized nominal return of 3.92% over a time when inflation averaged 2.4%. We can expect similar performance from these 2024 I Bonds.

My thinking: If market real yields remain high into the end of 2024, I will be looking to redeem — selectively — my remaining set of 0.0% I Bonds and some 0.1% versions to make gift-box purchases at 1.3%. I am in no rush to do this, because the 1.3% fixed rate will apply to all I Bond purchases through the end of October.

But what if real yields start declining, deeply? Then I will be definitely looking to make the swap to the 1.3% fixed rate because the November fixed-rate reset will be likely be lower than 1.3%.

At this point, there is no way to know. So just wait it out to October.

I am not a fan of stacking 10+ sets of gift-box swaps, because that will lock up the money for future distribution. One of the advantages of I Bonds is the ability to redeem after one year. But no one can redeem an I Bond that can’t be delivered because of the purchase cap.

Another option. If you are committed to redeeming low-fixed-rate I Bonds to buy the 1.3% version later this year, you could redeem now, place the proceeds in a money market account or in rolling 4-week T-bills earning 5.5% and then use that cash to buy the I Bonds in October, or possibly November.

You’d probably earn more than the 2.96% variable rate for several months. But there are two negatives to this strategy: 1) You will owe 2024 federal taxes on the interest earned, and 2) There is a slim chance that short-term yields could fall off sharply in the next few months.

Here’s a decent summary of the situation from CNBC, which includes (of course) a financial adviser telling you to sell your I Bonds:

If you need the money …

I keep stressing that the proper approach to I Bonds is to build a large reserve of inflation-protected, tax-deferred cash. At some point, you should start spending that money, either in retirement or to achieve other life goals. If you need the money, target the lower-fixed-rate I Bonds for the first redemptions.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I made a small addition to my TIPS at auction, and the real yield works for me. I didn’t watch…