By David Enna, Tipswatch.com

With Wednesday’s release of the March inflation report, the buying equation for U.S. Series I Savings Bonds became a bit clearer. We now know the I Bond’s variable rate will fall from the current 3.94% to 2.96% at the May 1 reset.

That’s a big drop. Does it make I Bonds unattractive? I don’t think so, and the reason is the I Bond’s current fixed rate of 1.3%, the highest in more than 16 years. But the fixed rate will also reset on May 1. So there is the key question: Where will the Treasury reset the fixed rate?

Confused? This is fairly simple. An I Bond is a Treasury security that earns interest based on combining a fixed rate and an inflation rate.

- The fixed rate will never change. So if you bought an I Bond in 2014 with a fixed rate of 0.2%, it will continue to have a 0.2% fixed rate for the life of the bond. Purchases through April 29, 2024, have a permanent fixed rate of 1.3%.

- The inflation-adjusted rate (often called the variable rate) changes each six months to reflect the running rate of inflation. That rate is currently set at 3.94% annualized and will drop to 2.96% after May 1. All I Bonds will eventually get the 2.96% variable rate, with the start date depending on the original month of purchase.

- The composite rate is a combination of these two rates, currently 5.27%, annualized, for a full six months for any bond purchased through April 2024.

Projecting the fixed rate

The following projection results from an inexact science, and in fact is simply a guess based on a decade of observations. The Treasury has never revealed an exact formula for setting the fixed rate, but it has noted that current trends in real yields are a factor. TreasuryDirect provides this cryptic information:

The Secretary of the Treasury, or the Secretary’s designee, determines the fixed rate. The rate is based on market rates that have been adjusted to account for the value of components unique to savings bonds. These include the early redemption put option, tax deferral feature, deferred purchase feature, and Treasury’s administrative costs.

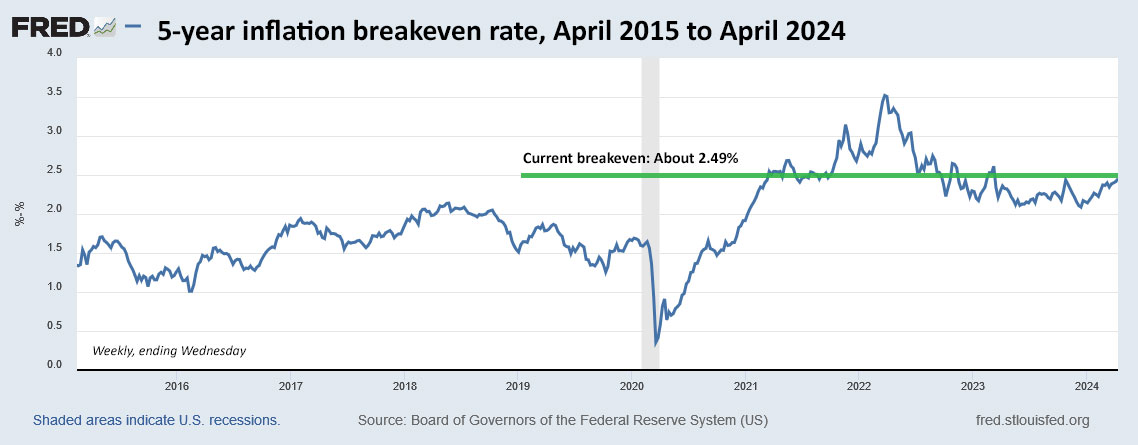

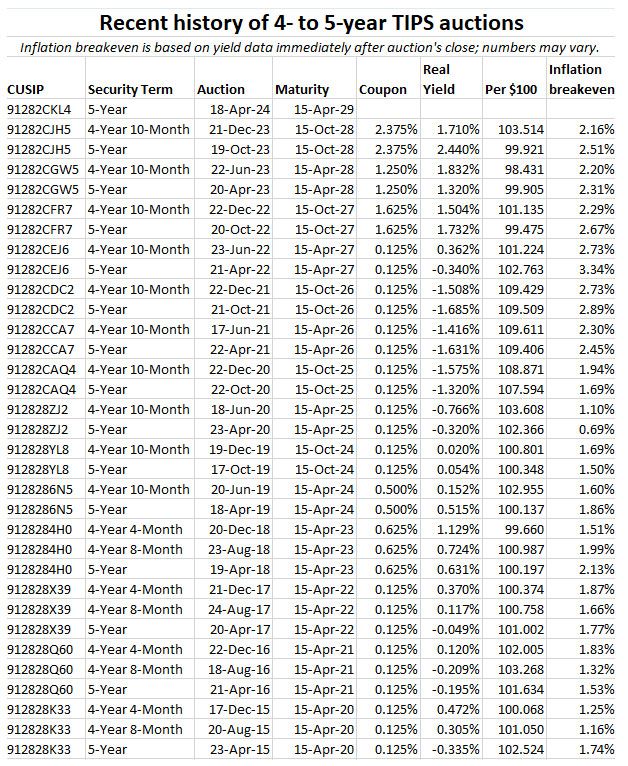

Based partly on feedback from Boglehead geniuses, I have settled on looking at the half-year average of the real yields of 5- and 10-year Treasury Inflation-Protected Securities as the best indicator of the next fixed rate. I then apply a ratio of 0.65 to the average. In recent years, this has been pretty accurate, as shown in this table:

In most cases, the 0.65 ratio has been on target, especially when applied to 5-year TIPS real yields. The May to October 2017 period is interesting, because the 5-year average was much lower than the 10 year, and the Treasury set the rate lower to match the 5-year average.

The Treasury always sets the fixed rate to a tenth decimal point, and my May 2024 projections are currently at 1.25% and 1.26%, with two weeks of data still to come. My conclusion (OK, guess) is that the Treasury will set the I Bond’s new fixed rate at either 1.2% or 1.3%.

But, as I always say, “The Treasury sometimes does weird things.”

What does this mean?

I Bond purchases are limited to $10,000 per person per year unless you use your tax return to get paper I Bonds (a bit late for that strategy) or add to your holdings through gift-box, trusts, or business-owner strategies.

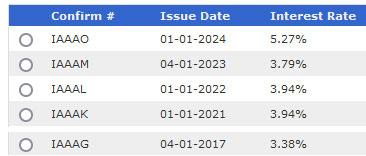

In my opinion — and I know some readers disagree — April’s higher variable rate (3.94% vs. 2.96%) and the locked-in 1.3% fixed rate make purchasing I Bonds to the limit in April the wiser choice. For that reason, I already purchased to the limit in March and have scheduled a gift-box set for purchase on April 25.

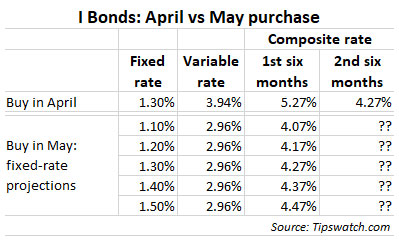

In this chart I have included some potential fixed rate changes, ranging from 1.10% to 1.50%. The most likely results are 1.20% or 1.30%, but anything can happen. By buying in April, you guarantee that your investment will earn 5.27% for six months and 4.27% for six months, or around 4.8% for the year.

Buying in May drops the likely return to 4.17% or 4.27% for the first six months, and then an unknown return for the next six months, depending on inflation from April to September 2024.

If the fixed rate is set at 1.50%, the buyer in May will be the winner in the long run. I personally like the certainty of the April purchase.

If you want to purchase in April, you can go into TreasuryDirect at any time and schedule the transaction. I recommend setting the date at April 25 or 26 to give Treasury time to complete the transaction in April. If you wait until April 30, your I Bond will be issued in May.

The rollover strategy. With the variable rate dropping to 2.96%, I Bonds with a fixed rate of 0.0% will be paying 2.96% for six months. That’s below market, and some investors may want to redeem any I Bonds with 0.0% fixed rates and roll that money over into the 1.3% April version, either through new purchases or the gift-box strategy. I discussed that strategy in a March 31 post.

Or, just hold? I’ve always stressed that the best I Bond strategy is to continue building your stockpile, until you have an amount that would work as a “large” emergency spending resource in retirement, all tax-deferred and inflation protected. If you are in the accumulation phase, just keep the 0.0% I Bonds and add the 1.3% version. And then, someday, use this as a spending account when needed.

Wait until October or November? Some readers have speculated that real yields could continue rising through 2024, making a higher fixed rate likely later in the year. That could happen. It’s iffy. But one advantage of a higher rate reset in November is that the fixed rate would carry over to January 2025, when the purchase limit resets.

Are I Bonds that attractive?

With short-term T-bill and money market rates topping 5%, many investors are shunning I Bonds because of the potentially lower nominal return plus the three-month interest penalty for redemptions within five years. Some thoughts:

- We just went through a phase of inflation hitting 40-year highs, and higher prices seem to be stubbornly hanging on nearly two years later. Inflation protection, for part of your portfolio, looks like a wise choice.

- Eventually, the Federal Reserve would like to start cutting short-term interest rates and then the T-bill and money market returns will begin falling. Some banks have already started lowering rates on high-yield savings accounts.

- I Bonds, if held for 5 years, create an inflation-protected store of cash you can use for future needs, with no penalty for redemption except for federal taxes on the interest.

Is this a short-term investment? I Bonds aren’t a good choice for money you will need in the next one or two years. You can get a 2-year Treasury note paying about 4.9%. That nominal return is likely to beat the return of an I Bond after the three-month interest penalty is applied.

Aren’t TIPS the better choice? There is an auction of a new 5-year TIPS this week and the real yield to maturity looks likely to be close to, or top, 2.0%. It could have a 70- to 80-basis-point advantage over the I Bond with a fixed rate of 1.3%. So yes, I think TIPS with real yields in the 2.0% range are more attractive. But many investors shun TIPS because of the complexity, and I Bonds have advantages of tax-deferred interest, a flexible maturity, and rock-solid deflation protection. I continue to invest in both.

Is inflation really a problem? The risk is there. Investments in TIPS and I Bonds provide insurance against unexpectedly high inflation, such as we saw in June 2022 when annual inflation rose to 9.1%. If inflation suddenly drops off, inflation-protection may slightly under-perform, but investors are still winners because no one wants high inflation.

I welcome your thoughts.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I made a small addition to my TIPS at auction, and the real yield works for me. I didn’t watch…