By David Enna, Tipswatch.com

One hour after I was reading a Bloomberg report on inflation steadily easing in future months, the Bureau of Labor Statistics sent out a December surprise: Seasonally-adjusted inflation rose rose 0.3% for the month and 3.4% for the year.

Both those numbers were higher than expectations, and the same was true for core inflation, which removes food and energy. For the month, core inflation also rose 0.3% and ended 2024 at 3.9%.

This should be a bit of a shock to the U.S. stock market, which recently seems to have been celebrating the return of U.S. inflation to the Federal Reserve’s target of 2.0%. But the December report sent a different message: Inflation isn’t quite tamed yet.

This report sets the official 2023 U.S. inflation rate at 3.4%, down dramatically from the 6.5% of 2022 and 7.0% of 2020. But before that, inflation had not reached this level since 2005.

The BLS noted that shelter again was the key cause of higher inflation, with costs rising 0.5% for the month and 6.2% over the last year, and accounting for more than half of the all-items increase. More from the report:

- Gasoline prices crept 0.2% higher for the month but were down 1.9% for the year.

- The costs of food at home rose 0.1% and were up a moderate 1.3% for the year.

- The index for meats, poultry, fish, and eggs rose 0.5% in December, led by an 8.9% increase in the index for eggs.

- Electricity costs rose a sharp 1.3% for the month and were up 3.3% for the year

- Costs of used cars and trucks rose 0.5% in December but were down 1.3% for the year.

- New vehicle costs rose 0.3% for the month and 1.0% for the year.

- The motor vehicle insurance index rose 1.5% in December and was up a whopping 20.3% in 2023.

- Costs of transportation services rose 0.1% for the month but were up 9.7% for the year.

- The index for rent rose 0.4% for the month and 6.5% for the year.

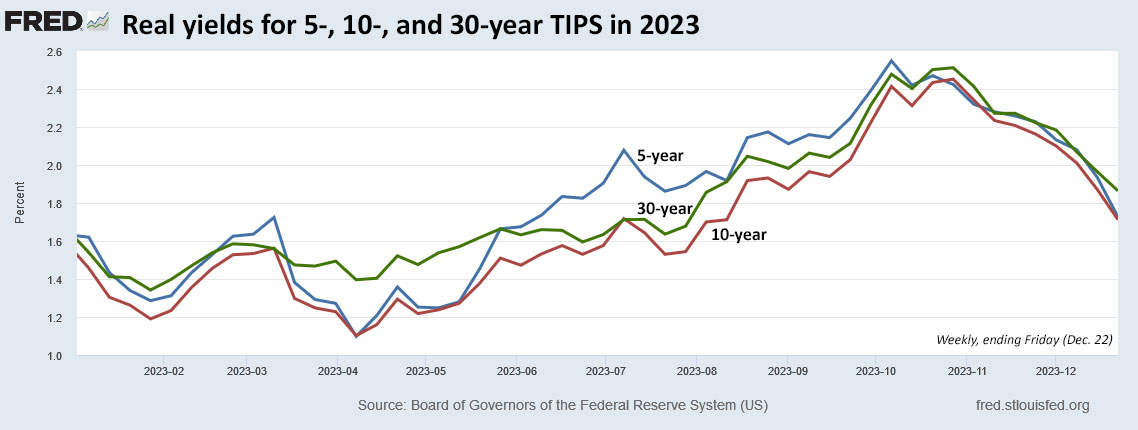

Here is the trend in 2023 for all-items and core inflation, showing that core inflation has been inching steadily lower, while all-items costs have fluctuated:

What this means for TIPS and I Bonds

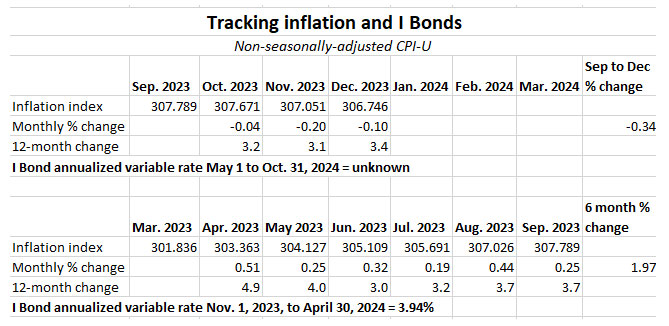

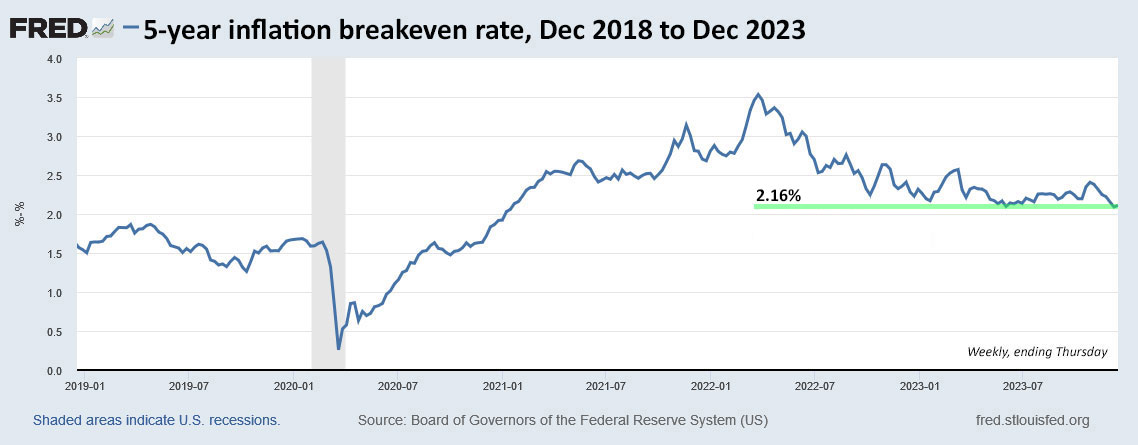

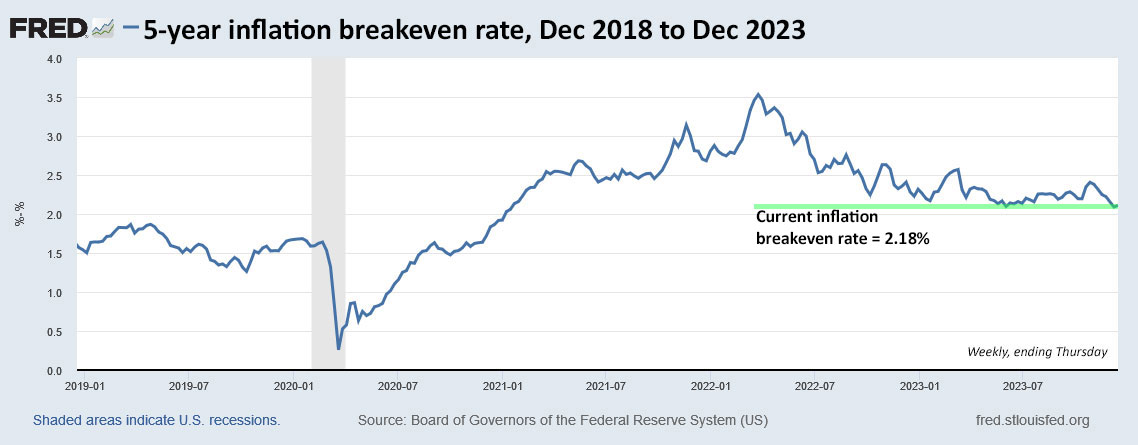

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates on I Bonds. For the month of December, the BLS set the inflation index at 306.746, a decrease of 0.10% from the November number.

Why was official inflation 0.3% and non-seasonal -0.10%? Keep in mind that seasonal and non-seasonal inflation balance out over the year and non-seasonal inflation tends to run lower from July to December and then higher from January to June. So expect a reverse of this trend beginning next month.

For TIPS. The December report means that principal balances for all TIPS will decline by 0.10% in February, after falling 0.20% in January. Here are the new February Inflation Indexes for all TIPS.

For I Bonds. The December report is the third in a six-month string that will determine the I Bond’s new variable rate, which will be reset on May 1 and eventually take effect for all I Bonds. So far, through three months, inflation has decreased 0.34%. The next three months are highly likely to reverse that negative number, but I would expect the end result to be less than 1.0%, which would result in a new variable rate around 1.72% for six months. Could it be higher? Maybe. Could also be lower. Lots can happen over the next three months.

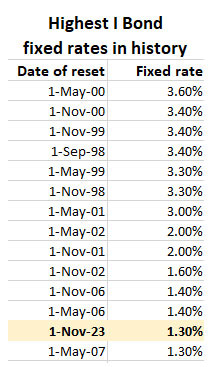

As I have noted before, long-term I Bond investors should focus on the fixed rate, which is currently 1.3% for any purchase through April. The fixed rate is permanent and is historically attractive right now.

Here are the relevant numbers so far:

What this means for future interest rates

I’d expect some turmoil in the Treasury market today, with yields rising higher. This inflation report was higher than expectations across the board. The report certainly should reinforce the Federal Reserve’s determination to hold interest rates steady until inflation shows signs of abating. But it probably won’t mean much in the long run: The Fed has signaled three short-term rate cuts in 2024 and I’d expect that to happen.

From a Bloomberg report this morning:

“Inflationary pressures, while generally inching lower, remain stubbornly higher than expectations as the so-called ‘last mile’ requires more time to reach the final goal. The last Fed minutes underscored that the path towards price stability remains uncertain, and today’s CPI report suggests that the Fed’s initial rate cut may be later than the market is hoping for.”

Quincy Krosby, chief global strategist at LPL Financial

“Today’s inflation report reinforces the notion that the market had gotten a little overexcited around the timing of rate cuts. These are not bad numbers, but they do show that disinflation progress is still slow and unlikely to be a straight line down to 2%.”

Seema Shah, chief global strategist at Principal Asset Management

So it is possible that we won’t see a rate cut from the Federal Reserve in March, as many had anticipated. Figure June, instead?

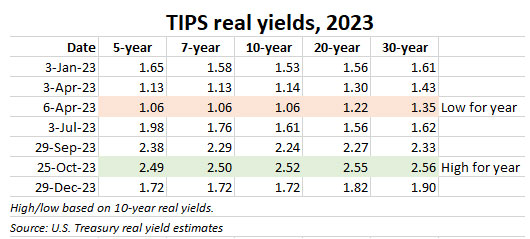

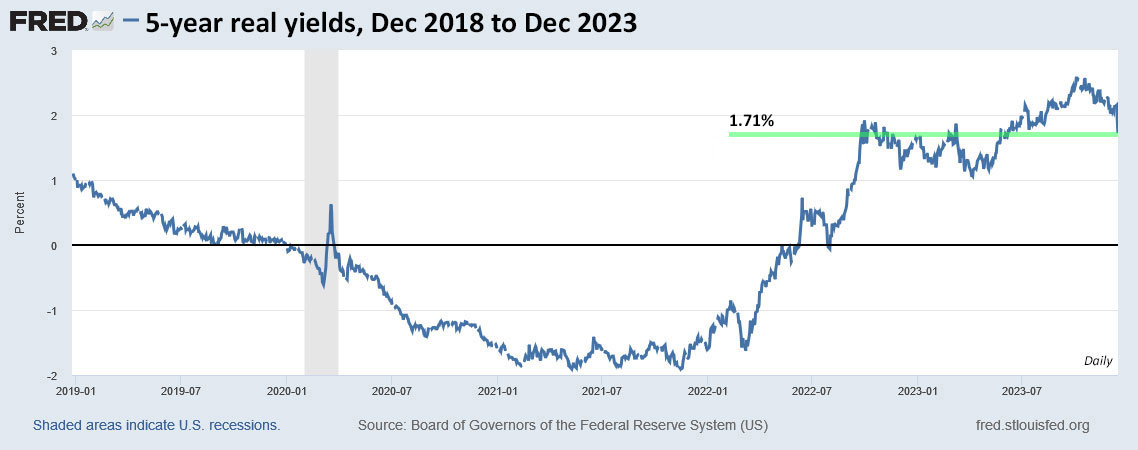

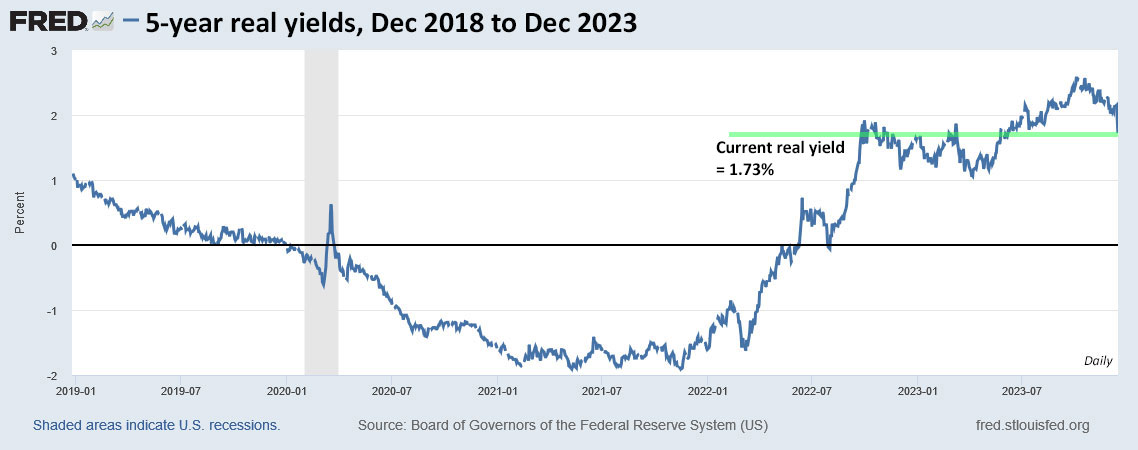

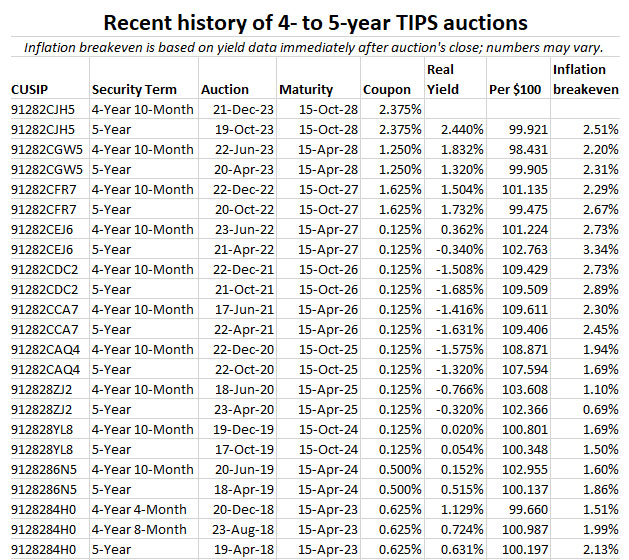

This December inflation report should hold real yields around current levels through the Jan. 18 auction of a new 10-year TIPS. I will be posting a preview article about that auction on Sunday morning.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I made a small addition to my TIPS at auction, and the real yield works for me. I didn’t watch…