Stock and bond markets are celebrating, with good reason.

By David Enna, Tipswatch.com

For the second month in a row, U.S. inflation came in below expectations in November, clearing the way for speculation that the Federal Reserve could soon pivot away from interest rate increases in 2023.

The Consumer Price Index for All Urban Consumers rose just 0.1% in November on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 7.1%. Both of those numbers were below expectations of 0.3% for the month and 7.3% year over year.

Core inflation, which removes food and energy, also came in below expectations, rising 0.2% for the month and 6.0% for the year.

The all-items increase of 7.1% was the smallest 12-month increase since the period ending December 2021, the BLS said. The core increase of 6.0% was the smallest since August 2021.

Obviously, this inflation report will be greeted with joy in the stock and bond markets, providing a clear signal that the Federal Reserve can set a path toward less-aggressive monetary tightening. Just a few minutes ago, I heard a Bloomberg commentator suggest that we need to revive the “transitory” description for U.S. inflation. Uh … let’s not get ahead of ourselves.

The BLS noted that the cost of shelter (up 0.6% for the month and 7.1% for the year) was the biggest factor in all-items inflation, more than offsetting a 2.0% decline in the cost of gasoline (which is still up 10.1% year over year.). Other highlights from the report:

- Food costs were up 0.5% for the month, continuing a string of sharply higher monthly price reports. Food at home costs are now up 12.0% year over year.

- The index for fruits and vegetables increased 1.4% in November, after falling 0.9% in October. On the positive side, the index for meats and poultry fell 0.2% for the month.

- Apparel costs were up 0.2% for the month and 3.6% for the year.

- The costs of medical care services fell 0.7% for the month.

- Costs for used cars and trucks fell for the fifth month in a row, down 2.9% for the month and 3.3% year over year (after rising sharply in 2021).

- Costs of new vehicles held stable, but are up 7.2% year over year.

- The index for airline fares fell 3.0% over the month, following a 1.1% decrease in October.

Overall, this was a positive inflation report, with the one exception of food prices, which are continuing to increase at a brisk pace. The cost of shelter, also higher, is considered a lagging indicator of past price increases rolling into effect. Shelter costs could eventually begin to fall in 2023.

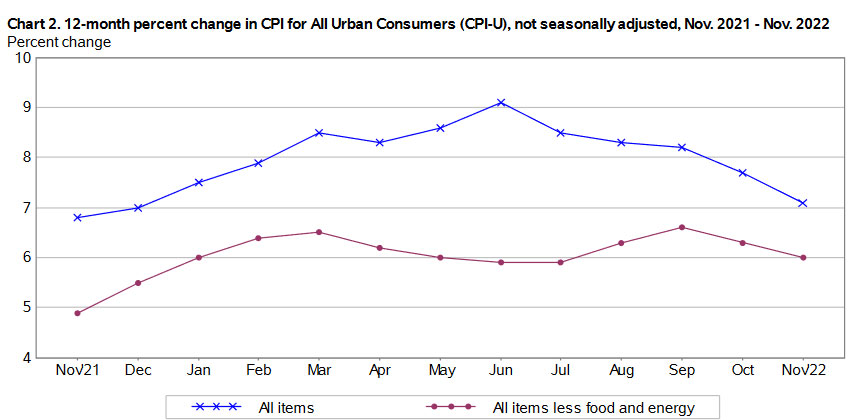

Here is the trend in all-items and core inflation over the last 12-months, showing the consistent declines in all-items inflation since early summer, drawing closer to core inflation as gasoline prices have declined:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates on I Bonds. For November, the BLS set the CPI-U inflation index at 297.711, down 0.1% from October.

For TIPS. The November report means that principal balances for all TIPS will decline 0.1% in January, after rising 0.41% in December. However, TIPS principal balances will have increased 7.1% for the year ending on January 31. Here are the new January inflation indexes for all TIPS.

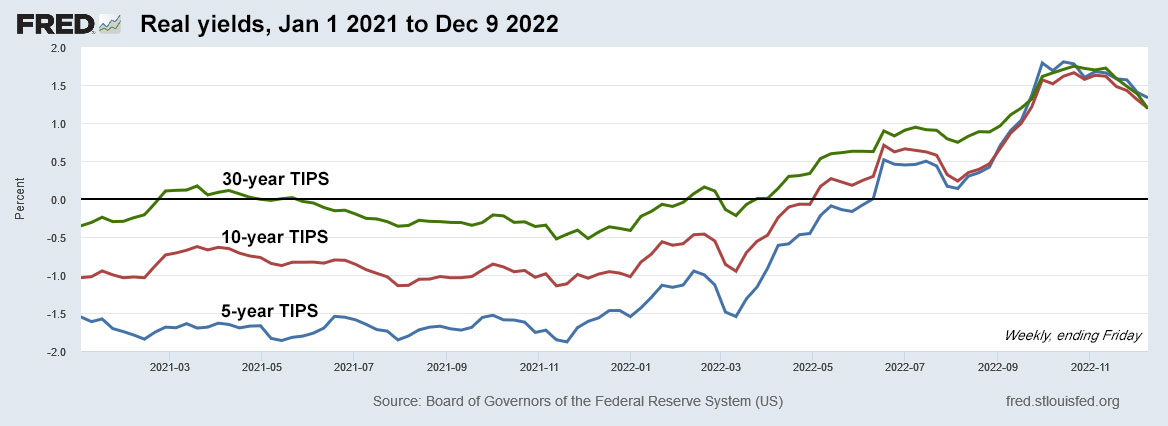

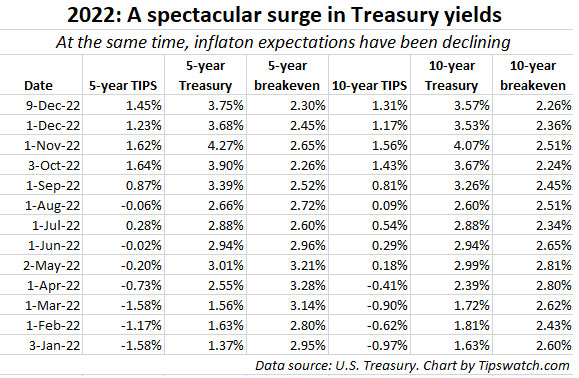

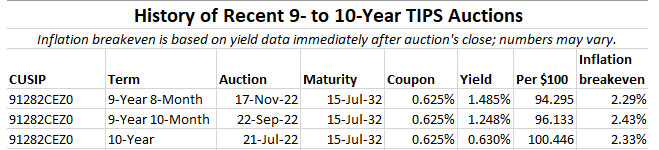

Today’s report is sending real yields down sharply, which could affect the Dec. 22 reopening auction of CUSIP 91282CFR7, which two months ago auctioned with a real yield of 1.732%. This morning that TIPS is trading on the secondary market with a real yield of 1.27%.

For I Bonds. The November report is the second in a six-month string that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset on May 1 based on inflation from October 2022 to March 2023. As of November, inflation is up 0.3%, which translates to an variable rate of. 0.60%. But it’s far too early to say where inflation is heading over the next four months. Here are the numbers:

What this means for future interest rates

The U.S. stock market is set to open sharply higher in a few minutes, a predictable response to this inflation report. And in the bond market, yields are sharply lower. All of this is anticipating that weakening inflation will allow the Federal Reserve to gradually stall future increases in interest rates. I think the Fed will go ahead with a 50-basis-point increase tomorrow, but give dovish signals about future rate increases.

It’s impossible to say at this point that inflation has truly been “tamed,” but we will now be entering a phase where year-over-year comparisons should cause inflation to continue declining. In January 2022, non-seasonally adjusted inflation increased 0.84%; in February 2022, 0.91%; and in March 2022, 1.34%. It’s unlikely U.S. inflation in future months will match those numbers, so year-over-year inflation should continue to decline in early 2023.

The Federal Reserve appears to have a path ahead that will allow it to hold short-term interest rates near the level it announces tomorrow.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Dr Matt....Sell and buy options