I Bond’s new composite rate could exceed 5% at the November reset.

By David Enna, Tipswatch.com

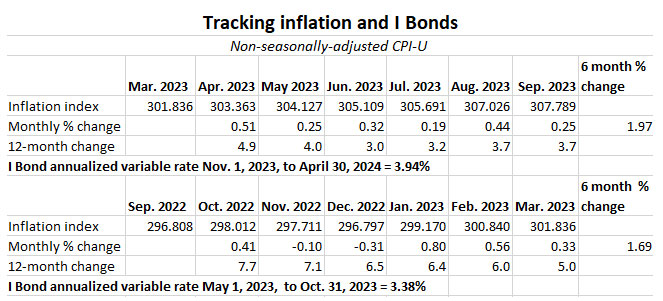

Investors in U.S. Series I Savings Bonds will see the investment’s annualized inflation-adjusted variable rate rise to 3.94% at the November 1 reset, up from the current rate of 3.38%, based on September inflation data released Thursday by the Bureau of Labor Statistics.

That variable rate, which is updated every six months, is applied to all I Bonds, no matter when they were purchased. The starting month of the change depends on the original month of purchase. The variable rate is combined with a permanent fixed rate to determine each I Bond’s composite interest rate.

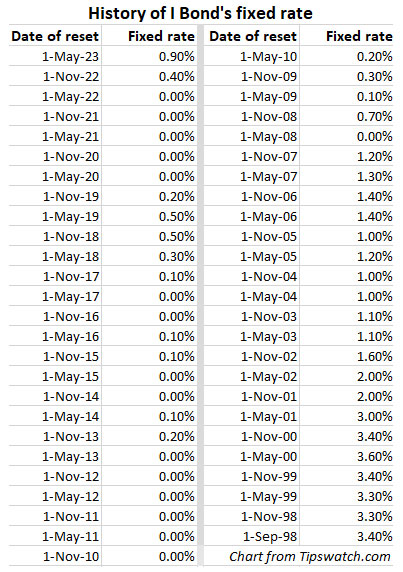

At the November reset, the I Bond’s fixed rate should rise above the current 0.9%, if market conditions stay stable through the end of this month. That means the new composite rate — for I Bonds purchased from November 2023 to April 2024 — should be higher than 5%, maybe as high as 5.4%.

But investors holding I Bonds with a 0.0% fixed rate will be getting an annualized return of 3.94% for six months.

The new variable rate was set by non-seasonally adjusted CPI-U from April to September 2023. The BLS set the September inflation index at 307.789, an increase of 0.25% over the August number. Here are the data:

A variable rate of 3.94% sets up a quandary for investors holding I Bonds with a fixed rate of 0.0% — and there were a lot of those issued over the last decade. In effect, 3.94% will be their new composite rate — more than 100 basis points lower than investments in federal money market funds or short-term T-bills.

Redeem or keep holding? My opinion: Hold if you want the inflation protection. But if this is a short-term investment, redemption probably makes sense.

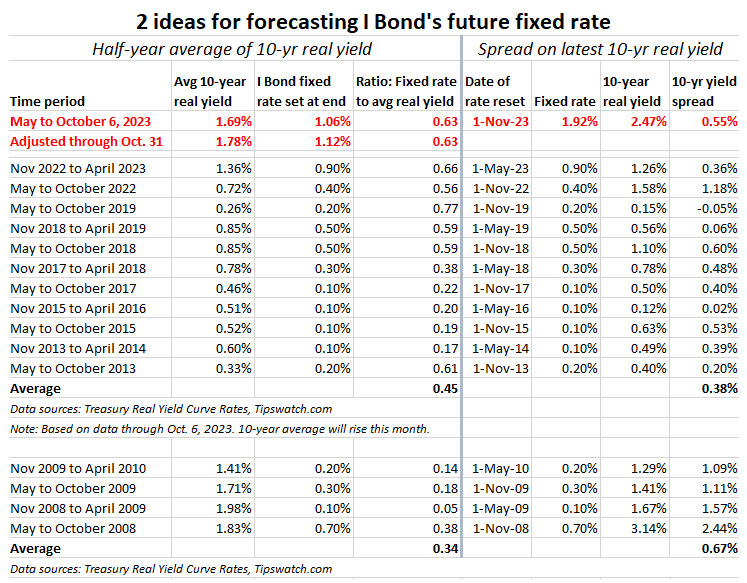

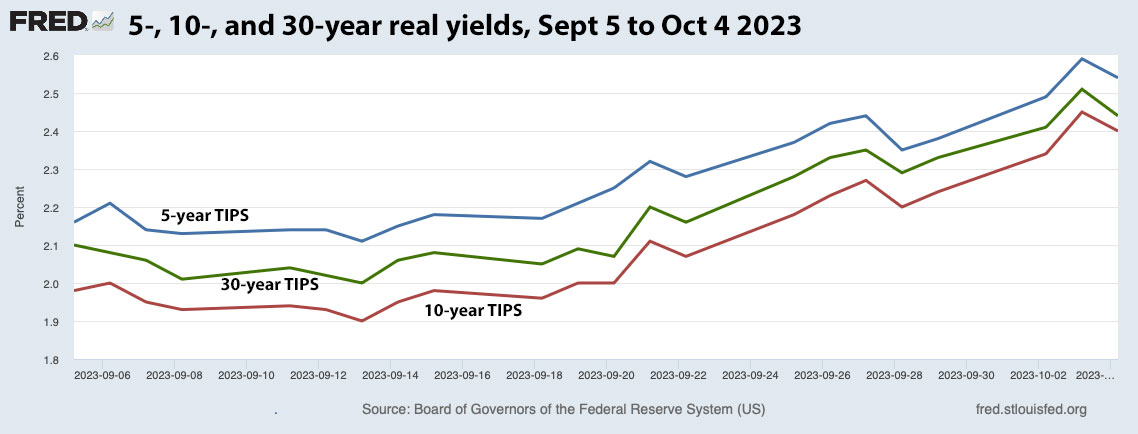

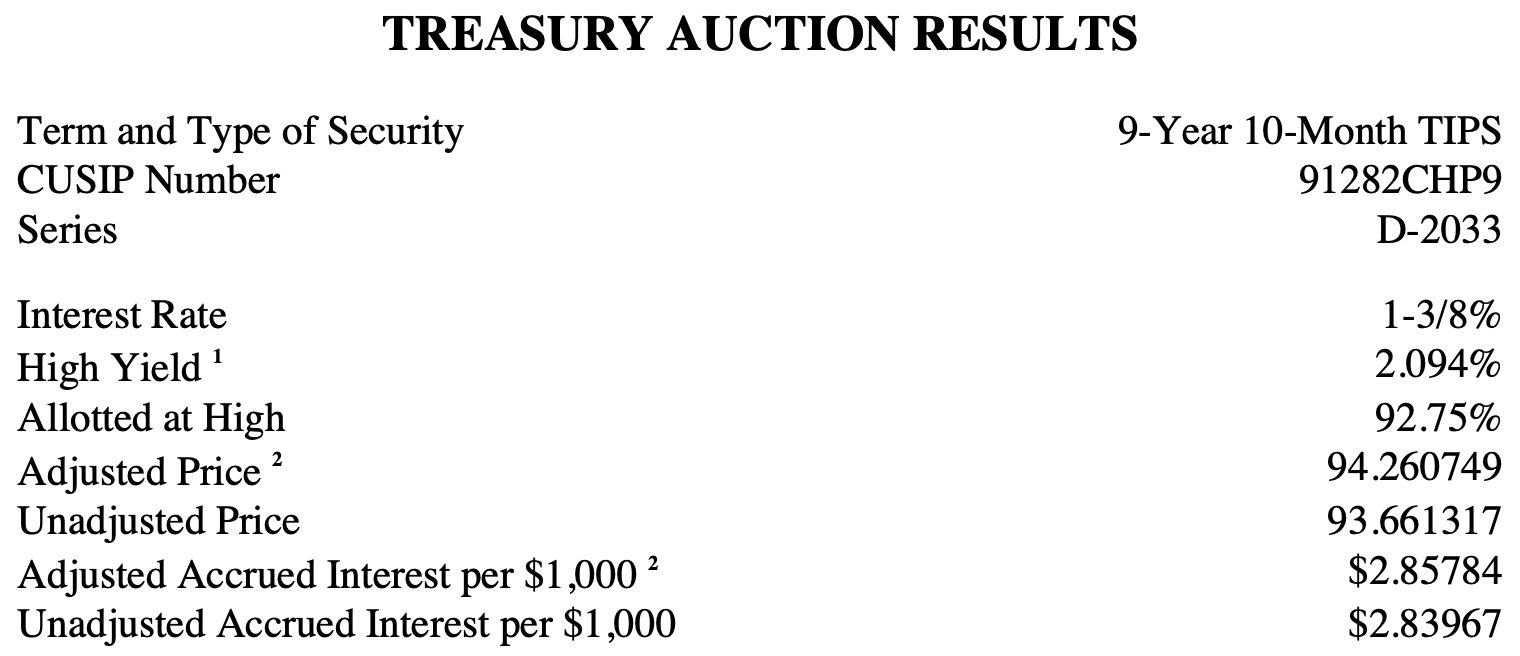

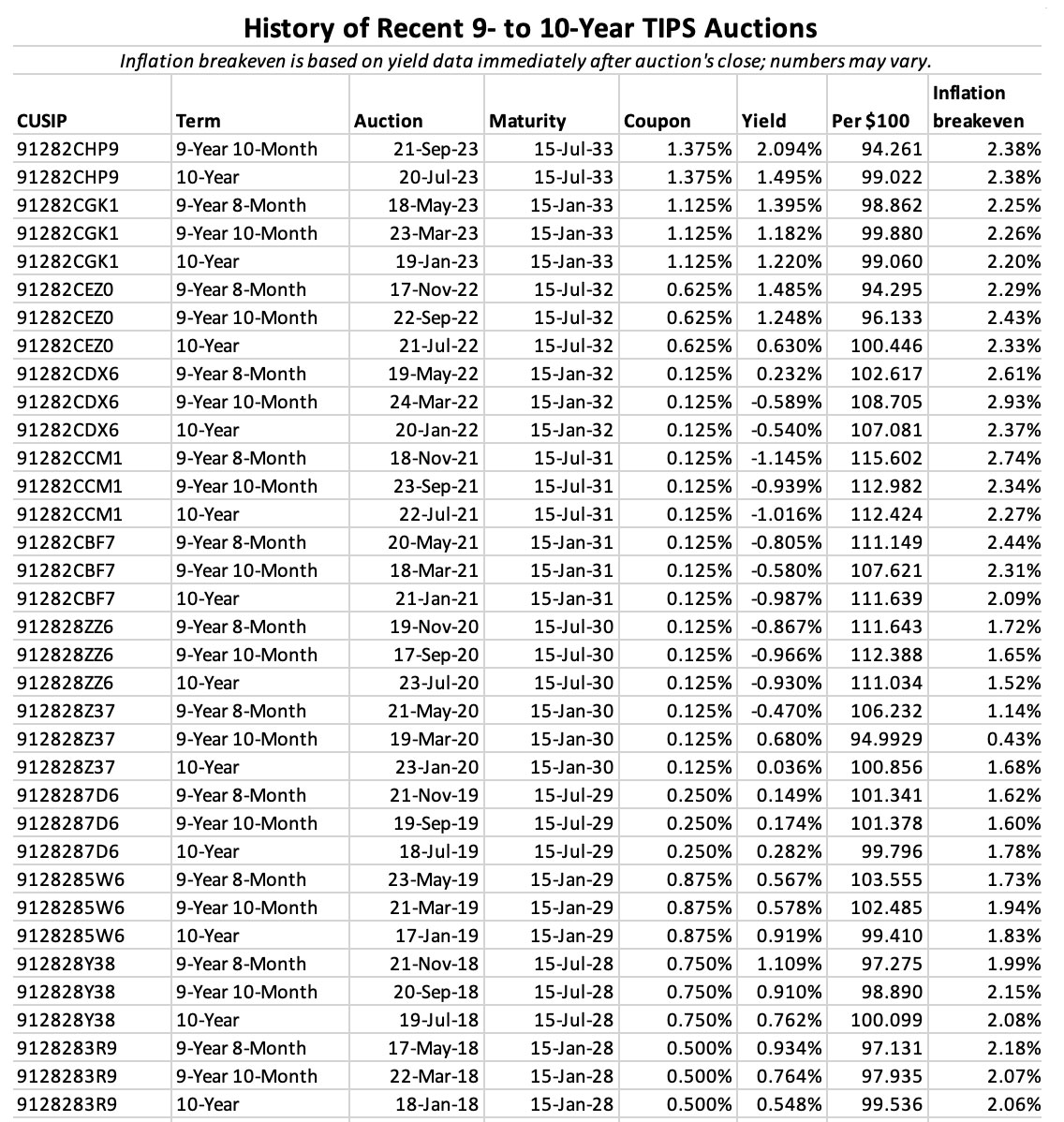

We don’t know what the new fixed rate will be for the I Bond at the November 1 reset. I have theorized that it could be the range of 1.4% to 1.7% (but this week’s real yield trends may indicate it will be lower). Any I Bond with a fixed rate above 1.0% will be attractive, in my opinion.

I will be writing more about this in coming days. But a quick thought: If the new I Bond fixed rate is 1.2% or higher at the reset, would I be a buyer in 2024? Absolutely, yes.

Social Security COLA

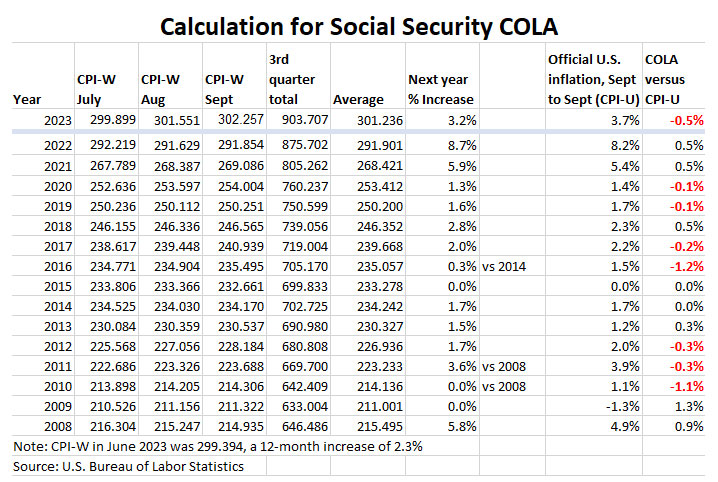

The September inflation report was the third of three — for July to September — that set the Social Security Administration’s cost of living adjustment for payments in 2024. The SSA uses a three-month average of a different index, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), to set its COLA.

For September, the BLS set CPI-W at 302.257, which produced a three-month average of 301.236, an increase of 3.2% over the same average for 2022. That means the Social Security COLA will be 3.2% for payments beginning in January. The numbers:

Note that the 2024 COLA of 3.2% trails the official U.S. inflation number of 3.7% for the September-to-September period. That is often the case, because the SSA’s formula using a three-month average tends to smooth out sharp increases in inflation. Also, CPI-W tends to run lower than CPI-U. But the increases for 2022 and 2023 payments actually outstripped official U.S. inflation.

Starting in January, the average monthly Social Security retirement benefit will rise by $59, from approximately $1,848 to $1,907, according to the SSA.

What this means for TIPS

Principal balances for Treasury Inflation-Protected Securities are adjusted each month based on non-seasonally adjusted inflation two months earlier. The September inflation index of 307.789 means that TIPS balances will rise 0.25% in November, after rising 0.44% in October. Here are new November inflation indexes for all TIPS.

September inflation

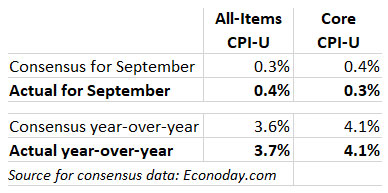

All-items U.S. inflation rose 0.4% in September and 3.7% year over year. Both of those numbers exceeded expectations. Core inflation, which omits food and energy, rose 0.3% for the month (less than the expected 0.4%) and 4.1% year over year (matching expectations).

So, nothing too surprising. The BLS noted that costs of shelter (up 0.6% for the month and 7.2% year over year) were a major factor in both all-items and core inflation. Gasoline prices were up 2.1% in September after rising 10.6% in August. Food at home costs rose a moderate 0.1% and are up only 2.4% over the year. Apparel costs were down 0.8% for the month.

Excluding housing and energy, services prices climbed 0.6% from August, the most in a year, according to Bloomberg calculations.

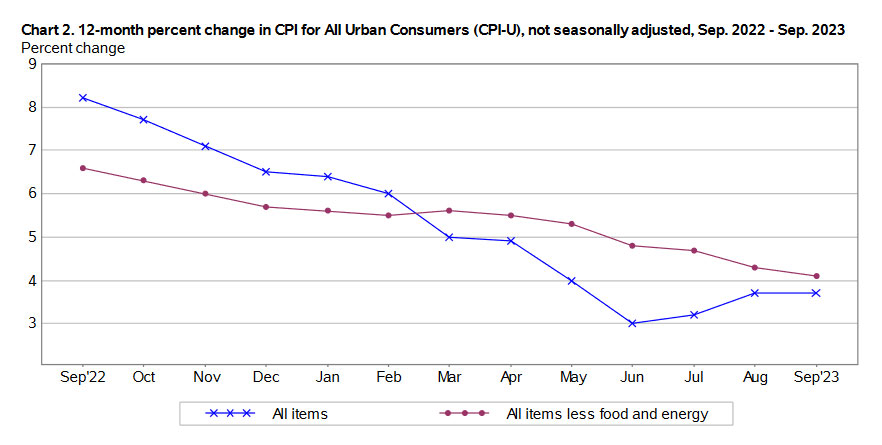

Here is the 12-month trend for all-items and core inflation, showing that all-items inflation has started climbing higher since June with increases in energy costs:

What this means for future interest rates

The Federal Reserve has been on a publicity campaign over the last 10 days to sell the idea that short-term interest rates “possibly” won’t need to go higher. Why? Because mid- and longer-term Treasury yields have been surging higher, causing the stock market to sell off. The bond market has been doing the Fed’s work.

But that interest-rate trend reversed a bit this week with turmoil in the Mideast and a flight to safety in U.S. Treasurys. Real yields have declined about 20 basis points this week. Still, I think the Fed will stick to the narrative that short-term rates have peaked but will remain elevated well into 2024.

Inflation is nowhere near the Fed’s target of 2.0%, with core inflation currently running at 4.1%. We’ve got a long way to go. From this morning’s Bloomberg report:

“While inflation is slowly edging lower, the strong labor market means that the threat of inflation resurgence cannot be ignored, keeping the Fed on its toes,” said Seema Shah, chief global strategist at Principal Asset Management. “The question around whether or not there will be one more interest rate hike is yet to be answered.” …

Anna Wong of Bloomberg Economics: “The September CPI report won’t convince most Fed officials that interest rates are sufficiently restrictive… Our baseline is for the Fed to hold rates steady for the rest of the year, but we see non-negligible risks of another rate hike, something the market is probably under-pricing.”

In other words, we face more uncertainty. And it is times like this that make investments with inflation protection highly desirable.

• I Bonds: A not-so-simple buying guide for 2023

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

—————————-

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Like most, most think there may be a legislative solution and what that may be...there could be no legislative solution!…