By David Enna, Tipswatch.com

This year, for the first time, I’ve soured on buying Treasury Inflation-Protected Securities at auction. Why? Because real yields have often come in a bit below “predicted” market value. That’s been especially true of the 10-year maturity:

- Jan. 19, 2023: A new 10-year TIPS – CUSIP 91282CGK1 — auctioned with a real yield to maturity of 1.22%, below the when-issued prediction of 1.26%. The coupon rate was set at 1.125%.

- March 29, 2023: That same TIPS reopened with a real yield of 1.182%. This auction was a winner, because premarket trading had it at 1.15%.

- May 18, 2023: The same TIPS reopened at 1.395%, below the premarket trading of 1.41%.

- July 20, 2023: A new TIPS — CUSIP 91282CHP9 — got a real yield of 1.495%, well below the when-issued prediction of 1.546%. The coupon rate was set at 1.375%.

For me, that last auction on July 20 was especially disappointing. (I was hoping for a coupon rate of 1.50% and just missed.) Now CUSIP 91282CHP9 will get its first reopening auction on Thursday. The results are likely to be much more attractive.

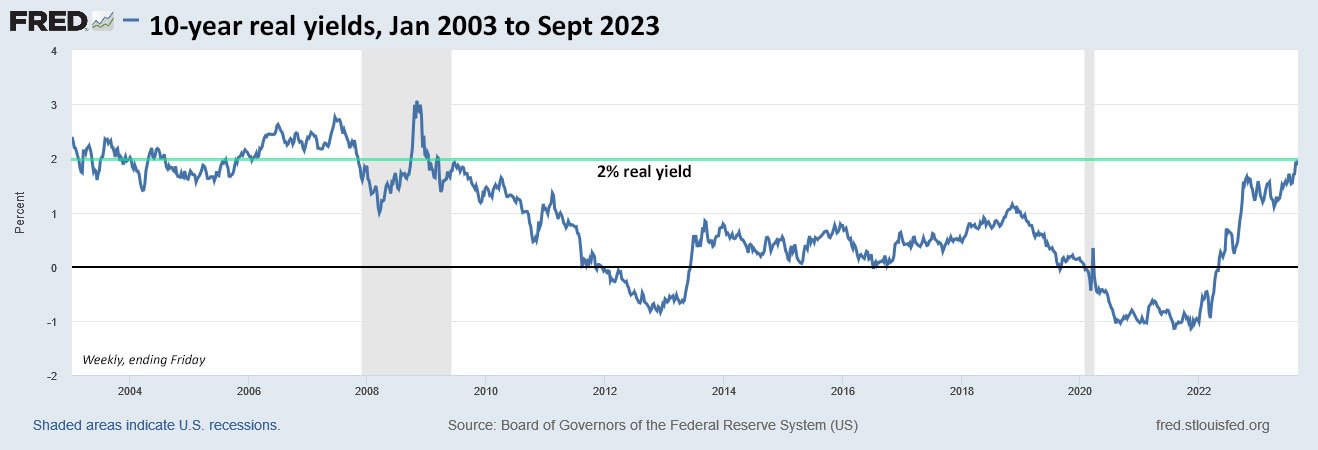

At Friday’s close, this TIPS was trading on the secondary market with a real yield to maturity of 1.98% — an increase of nearly 50 basis points in two months. And it is carrying a discounted price of 94.62. If that real yield holds, this auction will result in the highest 10-year auctioned real yield in more than 14 years.

But I won’t be a buyer, because I have filled the 2033 maturity on my TIPS ladder (with real yields of 1.22%, 1.40%, 1.495% and 1.964%). I’m done with 2033. My next purchase will be the 2034 TIPS to be auctioned Jan. 18.

If you are still working on 2033, this TIPS deserves a long look, either at auction or on the secondary market. You can check the current yield and price for this TIPS on the Bloomberg’s Current Yields page. Any real yield above 2.0% deserves consideration.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation each year until maturity.

Here is the trend in the 10-year real yield over the last 5+ years, a period that includes one dramatic period of Federal Reserve easing (March 2020 to March 2022), one mild period of Fed tightening (2018) and one aggressive period of tightening (April 2022 to today):

Pricing

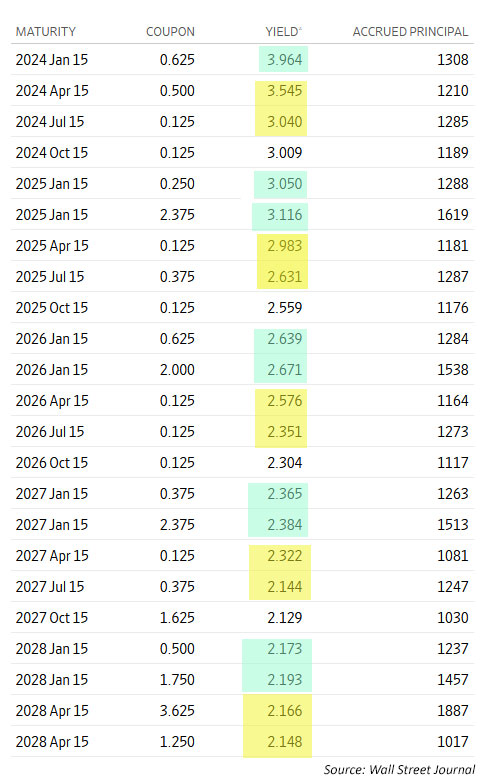

CUSIP 91282CHP9 will mature July 15, 2033. It has a coupon rate of 1.375%, well below the current market real yield of 1.98%, so it is selling at a substantial discount with a price of 94.62. This TIPS will have an inflation index of 1.00640 on the settlement date of Sept. 29.

What does this all mean for the price investors will pay? Let’s take a look at a potential $10,000 investment.

- Par value = $10,000

- Adjusted principal = $10,064 (based on the inflation index)

- Cost of investment = $9,523 (based on price of 0.9462)

- Accrued interest = About $28.40 (will be returned at first coupon payment)

- Total cost = $9,281

This is a rough estimate, of course, and is based on Friday’s closing value. Things can change before the auction closes at 1 p.m. EDT Thursday. You will find similar pricing on the secondary market, adjusted for a slight bid-ask spread and a slightly lower inflation index.

Inflation breakeven rate

With a nominal 10-year Treasury note currently yielding 4.33%, this TIPS has an inflation breakeven rate of 2.35%, close to the originating auction’s 2.38%. By historic standards, this is a high breakeven rate, but seems reasonable as the Federal Reserve struggles to move inflation to near 2.0%. For the last 10 years ending in August, U.S. inflation has averaged 2.8%.

Here is the trend in the 10-year inflation breakeven rate over the last 5+ years:

Note that inflation expectations have been gradually declining since last summer, when U.S. inflation peaked at 9.1%. The current rate is 3.7%, still well above the 10-year expectations.

Final thoughts

This is a strong offering, in my opinion. Over the last several weeks I have been pushing hard to fill out my TIPS ladder, which extends to 2043. My primary focus has been on getting real yields around 2.0% for the 2040 to 2043 period. I’d definitely be a re-buyer of CUSIP 91282CHP9 if my 2033 rung wasn’t full.

Can real yields continue higher? Definitely? Maybe? We don’t know. Getting real yields in the 2.0% range for extended maturities is attractive, so it’s a good time to act. It is a sensible purchase and shouldn’t be regretted.

Ponder this: As recently as March 2022, a 10-year nominal Treasury was yielding 1.74%. Now you can get 1.9% to 2.0% above inflation. The trend is good for TIPS investors.

What about secondary market versus auction? My advice is to watch the secondary market for yields you find attractive. That way you can know exactly what you are buying. The auction, however, is a good option for buyers of smaller lots because all investors get the high yield, without any spread.

If you are pondering an investment at Thursday’s auction, keep an eye on Bloomberg’s U.S. Yields page, which updates in real time. It is accurate, but any auction result can bring surprises. The auction closes at 1 pm EDT. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

By Thursday, I will be traveling in northern Greece so I can’t say for sure when I will be able to post the results.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Like most, most think there may be a legislative solution and what that may be...there could be no legislative solution!…