By David Enna, Tipswatch.com

Back on Oct. 8 I posted an article, “The I Bond’s fixed rate will rise. But by how much?” attempting to forecast the potential new fixed rate for the U.S. Series I Savings Bond, which will be reset by the Treasury on Nov. 1.

At the time, I noted one month of data remained — meaning through the end of October — and I warned that things change quickly in the financial markets. And of course, things did change, with the 10-year real yield initially falling from 2.47% on Oct. 6 to 2.29% a week later, before settling back to 2.44% at the market close on Oct. 26.

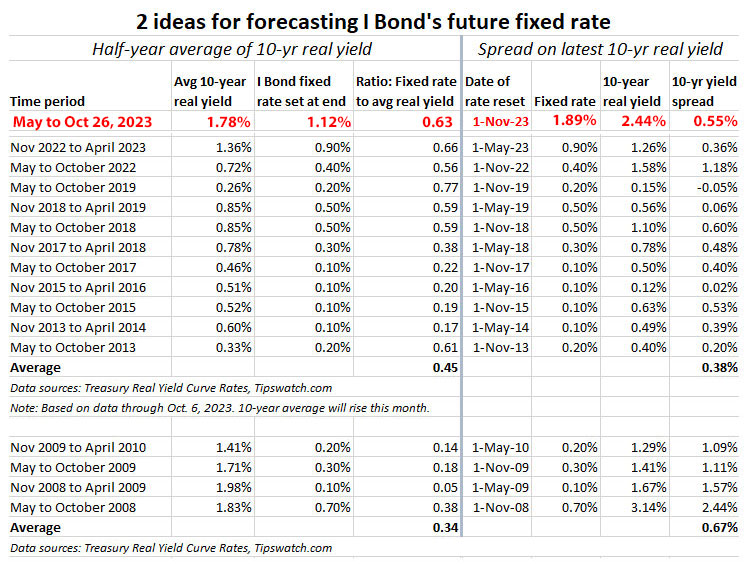

So here are my current projections, based on real yield data through October 26:

Half-year average: On the left is the projection using the half-year average 10-year real yield, which through Oct. 26 is 1.78%. This is the number I predicted in my earlier projection .

In the last five rate resets, the average ratio of fixed-rate to real yield has been 0.63. If you apply that to the 1.78% half-year average, you end up with a projection of 1.12% for the November 1 rate reset. Because the Treasury sets the fixed rate only to one decimal point, that could result in a fixed rate of 1.1% or 1.2%, above the current rate of 0.9%.

Latest 10-year real yield spread: The current real yield for a 10-year TIPS is 2.44%, much higher than the half-year average of 1.78%. This is because yields have surged nearly 50 basis points higher in the last two months.

In recent years, the typical spread between the fixed rate and the 10-year real yield has been in the range of 50 to 60 basis points. I used 55 basis points in this example. The result is a projection of 1.9% for the November 1 rate reset.

Conclusion

I believe the half-year real yield predictor (which is pointing toward a fixed rate of 1.1% to 1.2%) is a more reliable forecast. However, a fixed rate that low would be a massive 120+ basis points below the real yield of a 10-year TIPS, which would make I Bonds much less desirable in comparison.

So, if the Treasury sees this yawning gap, it should be willing to set the I Bond’s fixed rate a bit higher. Or not. Who knows?

I think right now we are heading toward a fixed rate in the range of 1.1% to 1.4%. That’s based partly on data, partly on “gut feeling.” Or possibly “wishful thinking”?

If the fixed rate ends up being 1.2%, the new composite rate will be 5.16%, below the nominal yield of a 1-year Treasury bill at 5.39%. This is a problem for short-term investors, which I addressed in my recent article, “Are U.S. Series I Savings Bonds losing their appeal?“.

What comes next

The last day you can buy an I Bond with a 0.9% fixed rate will be Monday, Oct. 30, because TreasuryDirect requires that purchases be made with one business day remaining to clear. Purchases on Tuesday, Oct. 31, are likely to be shifted to the new fixed rate (unknown) and new variable rate (3.94%).

So it is possible that the Treasury will announce the new fixed rate on the morning of Tuesday, Oct. 31. This early release is what it did at the May 1 reset and I think it is a good idea. Buyers should understand what they are purchasing.

By the way, standard practice for I Bond investors is to buy close to the end of the month because a purchase on any day of the month gets a full first month of interest. So there is no need to jump quickly into the new I Bond, no matter what the fixed rate is.

• I Bonds: A not-so-simple buying guide for 2023

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Like most, most think there may be a legislative solution and what that may be...there could be no legislative solution!…