But will it? The odds are better now. The data clearly support a higher fixed rate.

By David Enna, Tipswatch.com

How the U.S. Treasury sets the fixed rate on the Series I Savings Bond is wrapped in mystery. No one knows how or why. There is no formula. The Treasury says nothing except to announce the new fixed rate every May and November.

Right now, the common thinking in the I Bond community is this: “Demand for I Bonds is unusually strong and the Treasury doesn’t need to raise the fixed rate.” And, yes, this is true. But as a matter of fairness, the Treasury should raise the fixed rate, to reinforce the idea that an I Bond is a quality long-term holding for small-scale investors.

There is no question that demand for I Bonds is strong, triggered by the current annualized variable rate of 9.62%. This demand will probably continue into 2023 with a new variable rate somewhere around 6.2% to 6.4%. This is from a Barron’s article on the boom in demand in I Bonds:

“The average monthly issuance of $2.7 billion so far in 2022 compares with monthly sales of just $30 million in early 2021 when the rate was just 1.7%.”

The fairness issue

For short-term investors looking to swoop into very attractive I Bond rates for 12 to 15 months, a higher fixed rate doesn’t make much of a difference. But for investors looking to hold I Bonds for many years, a fixed rate above 0.0% is hugely attractive. Why? Because the fixed rate is permanent, staying with an I Bond for a full 30 years, or until it is redeemed.

That is why I say raising the fixed rate is an issue of fairness. While in the short-term a return of 9.62% is extremely attractive, the return on that I Bond is going to — eventually — track down with falling inflation. An I Bond with a 0.0% fixed rate has a “real yield” of 0.0% — meaning it will only track future inflation but not exceed it. That was fine over the last 2 1/2 years, when real yields on a similar investment — Treasury Inflation-Protected Securities — went deeply negative. But right now, 0.0% is a lousy real yield for a longer-term investor seeking inflation protection.

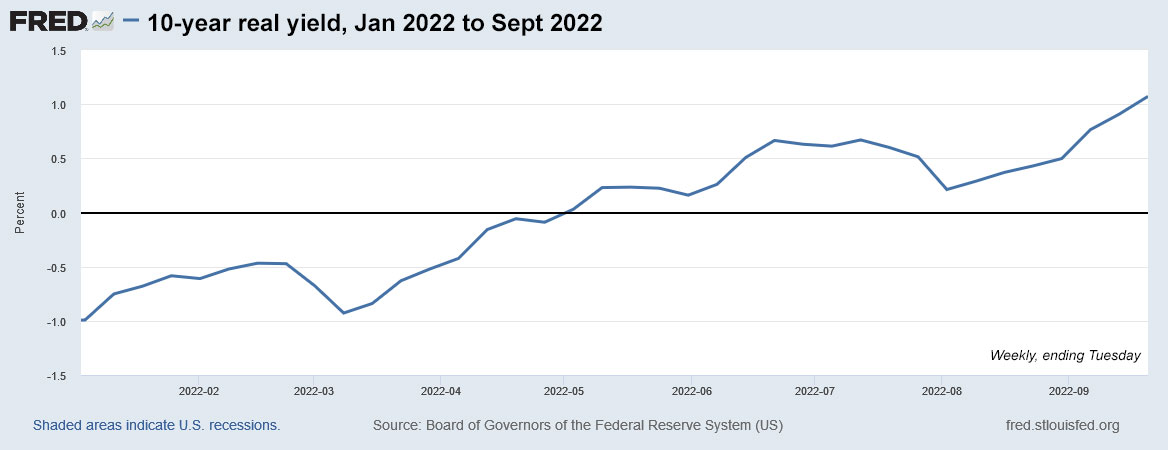

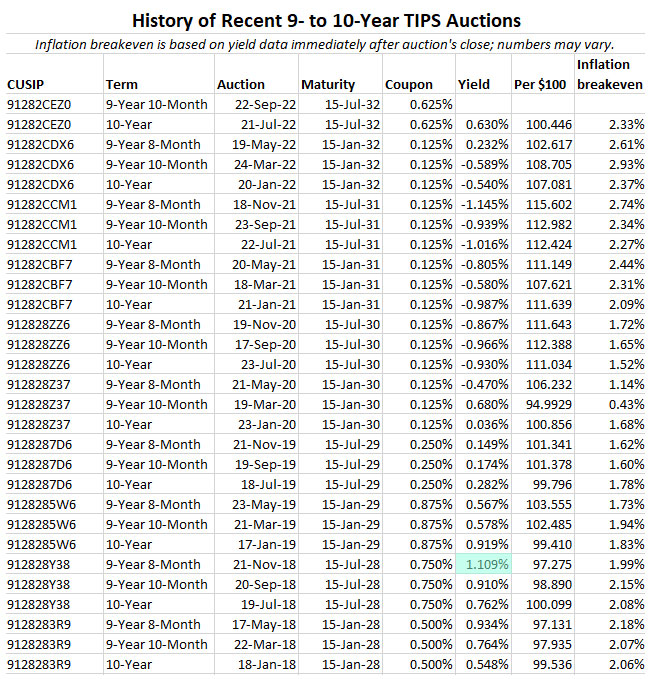

Here is the current real yield curve for TIPS, as estimated Friday by the U.S. Treasury:

Under “normal” circumstances — which admittedly have been rare over the last 12 years — the I Bond’s fixed rate tends to track 50 to 75 basis points below the real yield of a 10-year TIPS. I think that is fair, because I Bonds have several advantages: Tax-deferred interest, better deflation protection, ease of ownership and more efficient compounding.

Right now, however, the I Bond’s fixed rate of 0.0% is a stunning 168 basis points below the real yield of a 10-year TIPS. That makes TIPS — a more complicated investment — more attractive. The Treasury should recognize this and raise the I Bond’s fixed rate. I am going to suggest 0.3% to 0.5%. A 0.5% rate would put the fixed rate where it was in Fed’s last tightening cycle from November 2018 through November 2019. At that time, in November 2018, the 10-year TIPS had a real yield of 1.1%, much lower than it is today.

Here are the data I track on the spread in yield between the I Bond’s fixed rate and the 10-year TIPS real yield. (I used to also track the 5-year spread, but I found it wasn’t a reliable predictor.) In this chart I have highlighted in green the times when the Treasury raised the I Bond’s fixed rate above 0.0%.

There are some fairly large variations on this chart, but you have to go back to May 2009 to find a yield spread that approaches 168 basis points. Look at November 2019, when the Treasury set a fixed rate of 0.2% when the 10-year TIPS was yielding only 0.21%, a spread of just 1 basis point.

OK, I admit the variations could indicate the Treasury doesn’t even look at the 10-year real yield, and sets the I Bond’s fixed rate on demand alone. If that is true, then the fixed rate will continue at 0.0% from November 2022 to April 2023. But if the Treasury does look at the I Bond/TIPS yield spread — and it should — it will recognize the need to raise the I Bond’s fixed rate on November 1.

Why? Raising the fixed rate reinforces the idea that an I Bond is best used as a longer-term investment. The new crop of short-term investors will still be heading to the exits, most likely later in 2023. But I Bonds are a smart, sensible investment for capital preservation, ideal for the small-scale investor. The Treasury should reinforce that idea with a higher fixed rate that matches market trends.

Of course, this all depends on real yields holding at these high levels through October. Nothing is certain in today’s wild bond market.

• Confused by I Bonds? Read my Q&A on I Bonds

Hold off on buying I Bonds?

The obvious question will be … and here it comes … “Should I hold off on buying I Bonds until November to see if the fixed rate increases?” I believe that most of my readers have already bought I Bonds up to the $10,000 per person cap for 2022, so the question is moot. For others, it’s probably a toss up. If the fixed rate rises, you will be happy. If it stays at 0.0%, you miss out on 9.62% for six months.

And remember, if the fixed rate rises in November, it will be available for new purchases in January 2023, up to the $10,000 per person cap. So everyone wins.

I’d put the odds of a higher fixed rate at 50/50 at this point. Most people in the I Bond community believe the odds are much lower, but definitely above zero. We can’t ignore that TreasuryDirect has been overwhelmed this year by demand for I Bonds. Wouldn’t it be adding fuel to the fire by raising the fixed rate? Yeah, I see the dilemma.

But realistically, the fixed rate should be higher. So Treasury … do it.

An addendum, for the nerds …

In the comments I mentioned the Federal Register’s current regulations for I Bonds. Here is the link, which is often useful for understanding how I Bonds work.

Some quotes:

§ 359.10 What is the fixed rate of return?

The (Treasury) Secretary, or the Secretary’s designee, determines the fixed rate of return. The fixed rate is established for the life of the bond. The fixed rate will always be greater than or equal to 0.00% [1] . The most recently announced fixed rate is only for bonds purchased during the six months following the announcement, or for any other period of time announced by the Secretary.

Footnote: [1] However, the fixed rate is not a guaranteed minimum rate. The composite rate is composed of both the fixed rate and a semiannual inflation rate, which could possibly be less than the fixed rate or negative in deflationary situations. In all cases, however, the composite rate will always be greater than or equal to 0.00%.

§ 359.12 What happens in deflationary conditions?

In certain deflationary situations, the semiannual inflation rate may be negative. Negative semiannual inflation rates will be used in the same way as positive semiannual inflation rates. However, if the semiannual inflation rate is negative to the extent that it completely offsets the fixed rate of return, the redemption value of a Series I bond for any particular month will not be less than the value for the preceding month.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Dr Matt....Sell and buy options