13- and 26-week Treasury bills are an ideal way to maximize yield on your short-term savings. Here’s how to get started …

By David Enna, Tipswatch.com

When you get to be a certain age, cash becomes a lovely thing. Anyone who is retired and lacking steady income from work knows what I am talking about: It’s great to have a stockpile of cash to use for daily expenses and splurges like travel, but also for sudden disasters like the day two weeks ago when my 12-year-old KitchenAid dishwasher went dead.

I define cash as a safe investment — savings account, bank CD, federal money market account, U.S. Treasury bill — with a term of up to one year. But the problem over the last few years has been that safety also meant pathetically low returns, with yields typically topping out at 0.05% on money market accounts and maybe 0.2% in an online savings account.

For much of that time, inflation was very low, which held down the pain of very low yields. Now U.S. inflation is running at an annual rate of 8.6%, and looks likely to remain high for many months into the future. So there’s the dilemma: Where can we get better returns on our cash stockpile?

Let’s take a look at some possibilities, all very safe, in order of potential yield:

- 1-year Treasury bills, now yielding 2.79%

- 26-week Treasury bills, now yielding 2.62%

- 1 year bank CDs, typically yielding close to 2%

- 13-week Treasury bills, now yielding 1.73%

- 4-week Treasury bills, now yielding 1.27%

- Vanguard Treasury Money Market Fund, yielding 1.11%

- Online bank savings accounts, typically yielding 1% to 1.2%

- 6-month bank CDs, typically yielding 0.75% to 1%

- Fidelity Treasury Money Market Fund, yielding 0.98%

- 3-month bank CDs, typically yielding about 0.35%

I highlighted two investments in this list — the 13-week and 26-week Treasury bills — because I think they offer the best combination of safety, current yield, length of term and potential to adjust to higher yields as the Fed continues raising short-term interest rates.

For well over year, I’ve been holding cash in a T-Mobile Money banking account, which pays 4% on the first $3,000 invested (under certain circumstances) and 1% on the remainder. I wrote about this account back in July 2021 and I have been happy with it, because that 1% was at least 2 times what I could earn elsewhere. But now — sorry T-Mobile — 1% is no longer an attractive rate.

I like short-term Treasurys because these issues will react very quickly to any future rate increases by the Fed. You can easily schedule and stagger purchases on TreasuryDirect, and then have the investments roll over every 13 or 26 weeks, riding interest rates higher. The 13-week and 26-week Treasurys are auctioned every week, on Monday. (But it’s Tuesday this week because of the July 4th holiday.) This makes it very easy to stagger purchases to allow you to have access to your money on short notice.

For example, let’s say you have $60,000 in cash you want to put to work.

13-week Treasurys. You could make three purchases of $20,000 each, four weeks apart. Then you can roll these purchases over on TreasuryDirect, meaning you will always have access to $20,000 within about 4 weeks. Through the process, you will be riding interest rates higher if the Fed continues on its current course. Staggering 13-week Treasury bills is a good strategy for someone who might need the cash back in a short time.

26-week Treasurys. You could make three purchases of $20,000 each, eight weeks apart. Again you could roll these purchases over, riding interest rates higher, and always have access to $20,000 within eight weeks. Staggering 26-week Treasurys is a good strategy for someone who feels comfortable with a little longer delay in re-accessing the cash.

A combination. Put $30,000 in staggered 13-week Treasury bills, and $30,000 in staggered 26-week Treasury bills. You’d ride interest rates higher, get a slight yield boost for the 26-week term, and still have access to $10,000 within four weeks.

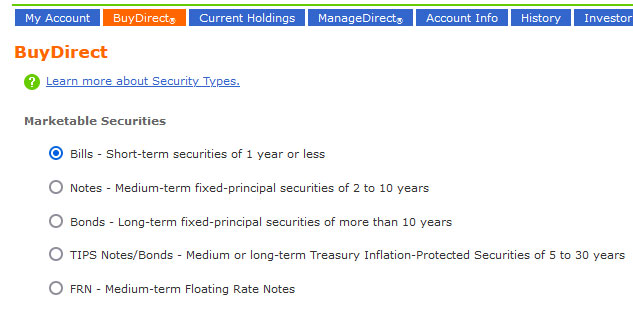

Scheduling these purchases on TreasuryDirect is simple, and I am assuming all my readers now have TreasuryDirect accounts because of the current I Bond mania. (If not, here’s my guide to opening an account.) Simply log into TreasuryDirect, and then click on BuyDirect in the top line of links. Here is what you will see:

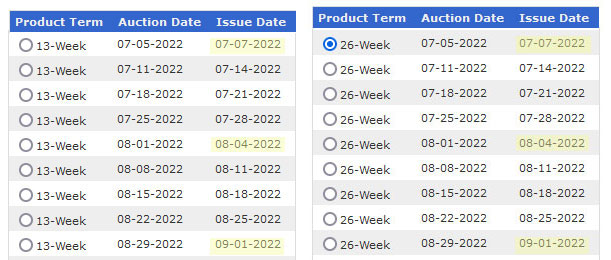

Click on Bills and then click Submit. That will take you to the full list of near-future auctions of Treasury bills, all with terms of 1 year or less. For the 13-week and 26-week Treasurys, you will see lists like these:

In this example, I have highlighted how you could stagger purchases of the Treasurys, but when you go to schedule a purchase, you have to enter each one separately. You can schedule purchases out two months on TreasuryDirect, and note that these issues auction each Monday and settle each Thursday.

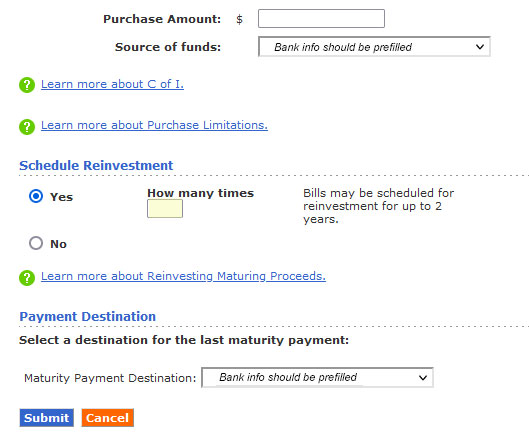

At the bottom of this page is where you enter the amount of each individual purchase, designate the source of the funds and note that you want to schedule reinvestments, and how many. Here is what that looks like:

Reinvestments can only be made for two years out, so that will limit you to 7 reinvestments of the 13-week bills, and 3 reinvestments of 26-week bills. To extend those reinvestments, you’d need to log into TreasuryDirect in the future and set them up. Also, when you need to retrieve the cash, you can log into TreasuryDirect at any time and cancel one or all your reinvestments. After maturity, the cash will return to your linked bank or brokerage account.

This strategy of rolling over short-term Treasurys will be most beneficial while the Federal Reserve is continuing to raise short-term interest rates. When the Fed stalls on rate increases or begins cutting rates, then you may want to look at investing elsewhere, or go with a longer-term Treasury or bank CD.

TreasuryDirect says you can schedule a reinvestment either when you buy your original security or up to four business days before the original security matures. Once you schedule a reinvestment, you can edit or cancel it within the same time frame.

How Treasury bills work

Treasury bills (often called T-bills) are a bit different than your standard bank account or CD. They are zero-coupon bonds, meaning an investor buys them at a discount to par value. Instead of paying a coupon interest rate, T-bills are eventually redeemed at par value to create a positive yield to maturity.

Here is what the auction result looks like, using the auction result for last week’s 13-week Treasury bill as an example:

In this auction, a person making a non-competitive bid (that is all of us little guys) got the high rate of 1.75% (annualized) and an investment rate of 1.782%. The investment rate extrapolates a higher annualized return if the proceeds are reinvested. The Treasury calls this the “equivalent coupon-issue yield.” An investor buying $10,000 of this T-bill would have paid about $9,955.76 and will get $10,000 at the Sept. 29 maturity.

These short-term Treasurys react very quickly to Fed rate increases. Two months ago, on May 9, a 13-week Treasury got an investment rate of 0.915%. Four months ago, on March 7, the auction got a rate of 0.386%.

When the T-bill reaches maturity and is not reinvested, TreasuryDirect will deposit the principal into your designated bank account. The deposit is made on the day the security matures.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

UrsaTaurus, I have been contemplating similarly, buying long without the expectation of holding to maturity (I will be dead). I…